Navigating the healthcare maze? Learn how to find the best health insurance in 2026. We break down plans, hidden costs, and expert tips to protect your wallet and health.

Table of Contents

Let’s be incredibly honest for a moment: nobody actually likes shopping for insurance. It is right up there with sitting in traffic or realizing your milk expired three days ago. You’re forced to stare at endless spreadsheets filled with terms like “actuarial value” and “coinsurance,” all while trying to predict exactly how sick or injured you might get over the next twelve months. It’s an overwhelming, high-stakes guessing game. Yet, finding the best health insurance is arguably one of the most important financial decisions you’ll make all year. One wrong turn could mean the difference between a small co-pay and a mountain of medical debt that sticks around longer than your college loans.

The reality of the 2026 healthcare market is that “cheap” can be very expensive. We often get seduced by a low monthly premium only to realize too late that the plan doesn’t cover our favorite doctor or our specific prescription. To find the best health insurance, you have to look past the sticker price and dive into the mechanics of how the plan actually works when life hits the fan. It’s about building a safety net that is strong enough to catch you, but flexible enough not to break your bank account every month.

The Myth of the “One-Size-Fits-All” Plan

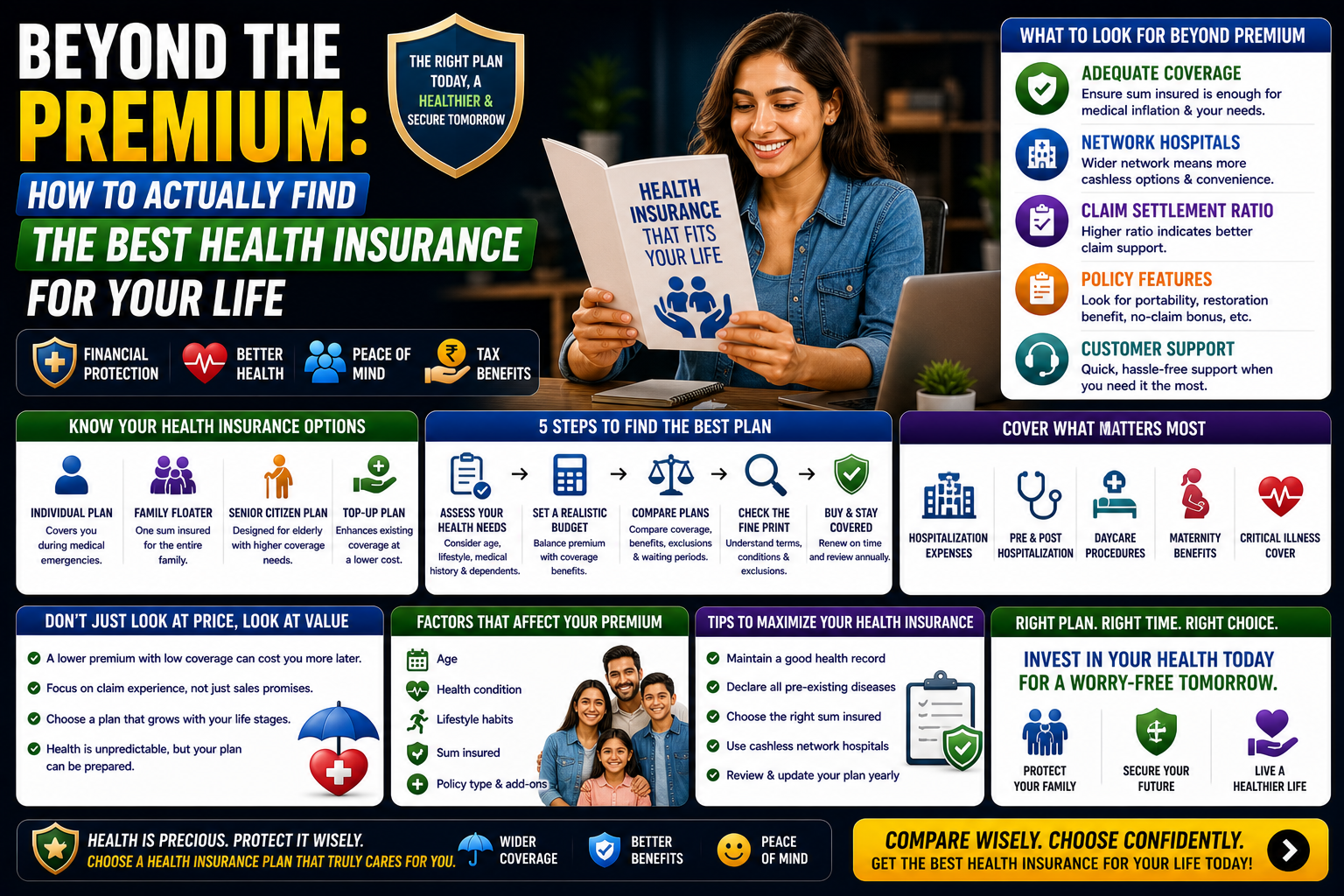

If there’s one thing I’ve learned from years of analyzing the insurance industry, it’s that the “perfect” plan is a total ghost. It doesn’t exist. What qualifies as the best health insurance for a twenty-something freelance graphic designer in Brooklyn is going to look a lot different than the best health insurance for a family of five in the suburbs of Austin.

You have to start by auditing your own life. Are you someone who visits the doctor once a year for a checkup, or do you have a chronic condition that requires monthly specialist visits? Do you play high-risk sports, or is your idea of a “workout” a brisk walk to the fridge? Your health profile is the compass that points you toward the best health insurance for your specific situation. If you’re healthy, a High Deductible Health Plan (HDHP) might be a brilliant move. If you have a family, a traditional PPO with a lower deductible is often the safer, more predictable bet.

Decoding the Alphabet Soup: HMO, PPO, and EPO

Before you can choose the best health insurance, you have to understand the “Network” you’re buying into. This is where most people get tripped up.

- HMO (Health Maintenance Organization): Usually the most affordable, but you’re locked into a specific local network and you need a “referral” for everything.

- PPO (Preferred Provider Organization): More expensive, but you have the freedom to see almost any doctor without a hall pass from your primary physician.

- EPO (Exclusive Provider Organization): A middle ground that doesn’t require referrals but generally won’t pay a cent if you go out of network.

When searching for the best health insurance, check the provider directory before you sign anything. If your trusted family doctor isn’t on the list, that “great deal” is going to feel like a massive headache the first time you need an appointment. You can find more detailed breakdowns on these structures via Wikipedia’s entry on Health Insurance in the US.

The True Cost: Deductibles vs. Out-of-Pocket Maximums

The monthly premium is just the “cover charge” to get into the club. To find the best health insurance, you need to look at the total “effective cost.” This means doing some math on your deductible—the amount you pay before the insurance company starts chipping in—and your Out-of-Pocket Maximum.

The Out-of-Pocket Maximum is the most important number on your policy. It is your “worst-case scenario” number. In 2026, many people are opting for plans with higher deductibles but lower out-of-pocket maximums. Why? Because they’d rather pay a bit more for a broken arm if it means they won’t lose their house if they face a major illness. The best health insurance provides a ceiling on your financial risk. If a plan has an unlimited or excessively high maximum, walk away. You’re not buying insurance at that point; you’re just gambling.

Leveraging the Health Savings Account (HSA)

If you decide to go with a high-deductible plan to secure a lower premium, you absolutely must look for an HSA-compatible option. For many, an HSA is the secret ingredient that turns a standard policy into the best health insurance strategy.

An HSA allows you to put away pre-tax money to pay for medical expenses. The money rolls over year after year, and in many cases, you can even invest it. It is essentially a “medical IRA.” If you stay healthy, that money grows. If you get sick, you’re paying with “untaxed” dollars, which effectively gives you a 20-30% discount on your healthcare costs. When people ask me about the best health insurance for long-term wealth building, the HSA-eligible plan is almost always part of the conversation.

The Rise of Telehealth and Digital Care

One major shift we’ve seen in 2026 is that the best health insurance providers are now doubling down on digital access. If your plan doesn’t include 24/7 “virtual visits,” you’re living in the past. Telehealth is a massive win for busy parents and professionals.

Being able to talk to a doctor at 2:00 AM from your phone for a simple prescription or a quick diagnosis is a game-changer. It keeps you out of the expensive Urgent Care center and saves you hours of sitting in a waiting room full of other sick people. As you compare options for the best health insurance, look at their digital interface. Is the app easy to use? Can you text a nurse? These “quality of life” features are what separate a mediocre plan from a great one.

Prescription Drug Coverage: The “Hidden” Budget Buster

I’ve seen it happen dozens of times: someone finds what they think is the best health insurance, only to realize their “Tier 3” medication isn’t covered or carries a $200 co-pay. Every insurer has a “Formulary”—a fancy list of drugs they cover and how much they’ll charge you for them.

If you take a regular medication, you must check the formulary of any potential plan. Some of the best health insurance companies offer “mail-order” pharmacy programs that can save you a fortune. Also, keep an eye on “step therapy” requirements, where the insurer forces you to try a cheaper drug before they’ll pay for the one your doctor actually prescribed. It’s a frustrating hurdle, but knowing about it ahead of time helps you navigate the system more effectively.

Mental Health and Wellness Benefits

In 2026, the definition of the best health insurance has expanded. It’s no longer just about broken bones and heart health. Mental health coverage has moved from an “extra” to a “must-have.”

Look for plans that offer a robust network of therapists and psychologists. Some of the best health insurance options even provide free subscriptions to meditation apps or gym memberships. These wellness perks might seem like fluff, but they contribute to your overall quality of life and can prevent more serious (and expensive) health issues down the road. According to the Centers for Disease Control and Prevention, preventive care is the most effective way to lower long-term medical costs.

Navigating the Open Enrollment Window

Timing is everything. For most people, you can only switch to the best health insurance during the Open Enrollment Period at the end of the year. If you miss this window, you’re stuck with your current plan unless you have a “Qualifying Life Event”—like getting married, having a baby, or moving to a new state.

Don’t wait until the final forty-eight hours to start your research. The sheer volume of information can lead to “analysis paralysis,” causing you to just pick the same plan you had last year. But insurance companies change their networks and their prices every single year. The best health insurance you had in 2025 might be a terrible value in 2026. A quick check of the new rates and network changes is mandatory if you want to protect your wallet.

FAQ Section

1. What is the average cost of the best health insurance in 2026? It varies wildly by state and age, but for a single adult, premiums typically range from $450 to $700 per month for a “Silver” tier plan. Keep in mind that federal subsidies can significantly lower this cost for many families based on income.

2. Is a PPO always better than an HMO? Not necessarily. While a PPO offers more freedom, an HMO can be the best health insurance for someone who is looking to save money and has a great local hospital system they are happy to stay within. It’s about the trade-off between choice and cost.

3. Does “Best” always mean most expensive? Absolutely not. The best health insurance is the one that provides the most coverage for the specific doctors and medications you use. A high-premium plan with features you never use is just a waste of money.

4. Can I get health insurance if I have a pre-existing condition? Yes. Thanks to current regulations, insurers cannot deny you coverage or charge you more for the best health insurance based on your health history. This is a foundational protection for all consumers in the 2026 market.

5. What is “Coinsurance”? Coinsurance is your share of the costs of a covered health care service, calculated as a percentage. For example, if your best health insurance plan has a 20% coinsurance, you pay 20% of the bill after you’ve met your deductible, and the insurance pays the rest.

6. How do I know if my doctor is in-network? The most reliable way is to call the doctor’s office directly and provide them with the specific name of the insurance plan. Online directories for the best health insurance are a great start, but they can sometimes be outdated.

Conclusion

At the end of the day, health insurance is about peace of mind. It’s about knowing that if life throws you a curveball, you have a partner in your corner who will help shoulder the financial burden. Finding the best health insurance requires a little bit of homework and a lot of honesty about your own health and habits.