Want to skip the stress of borrowing? Learn how the loan approval process works in 2026, from credit checks to final funding, and how to guarantee a “yes.”

Table of Contents

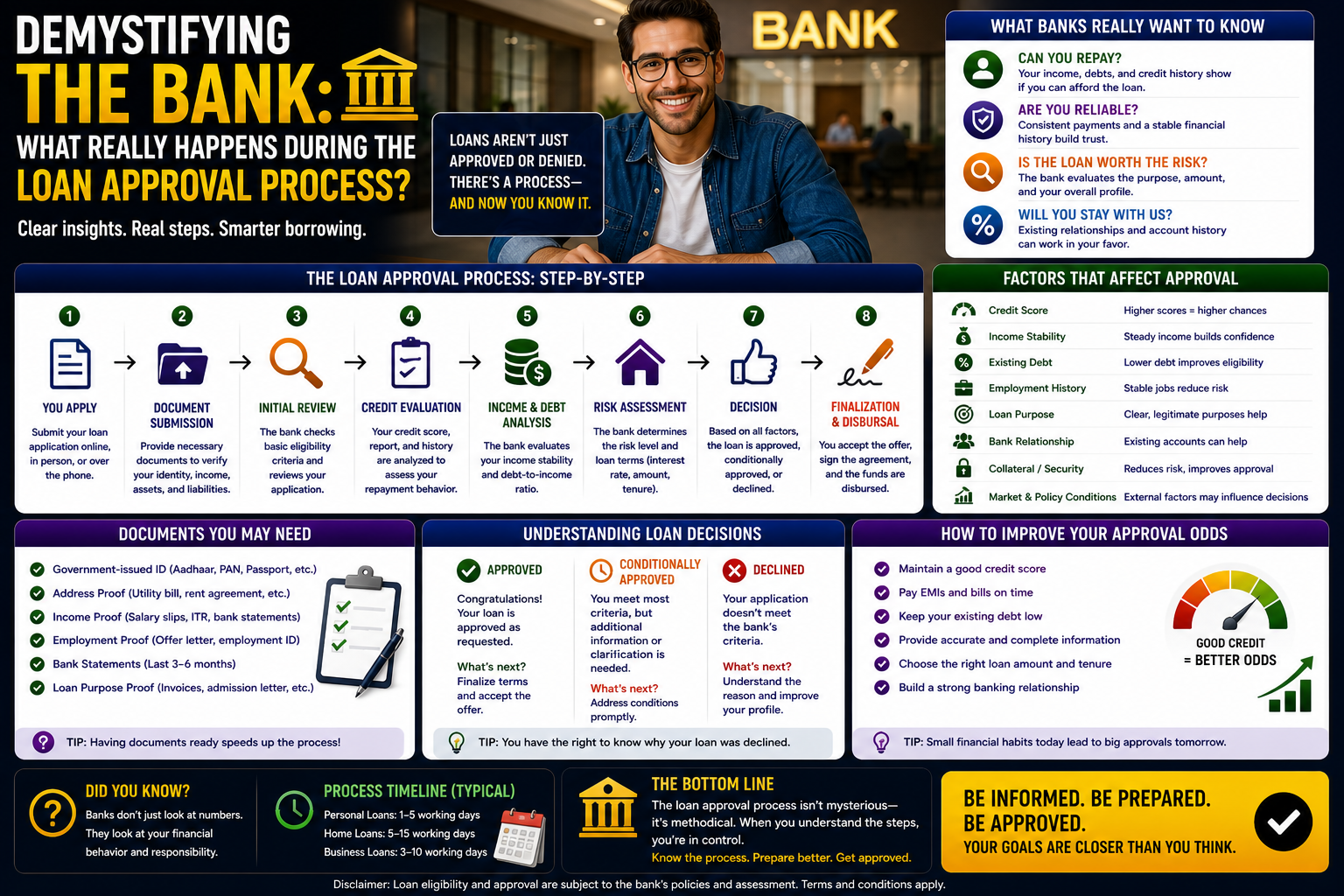

We’ve all been there—sitting across from a loan officer or staring at a “processing” wheel on a smartphone screen, heart racing just a little bit. Whether you’re trying to buy your first home, fund a small business, or simply consolidate some nagging credit card debt, that waiting period feels like an eternity. It’s a strange, vulnerable position to be in, essentially asking a giant institution to vouch for your future. But while it feels like a mysterious black box, the loan approval process is actually a very structured, logical sequence of events. If you understand the mechanics behind the scenes, you can stop feeling like a victim of the system and start acting like a partner in the deal.

The reality of 2026 is that banking has moved at lightning speed, yet the core questions lenders ask haven’t changed since the days of hand-written ledgers. They want to know: Can you pay it back? Will you pay it back? And what happens if you don’t? Navigating the loan approval process successfully is about providing clear, undeniable evidence for all three of those answers. It’s not just about having a high salary; it’s about the story your data tells. Let’s pull back the curtain on how banks actually decide who gets the cash and who gets the “thanks, but no thanks” email.

The First Look: Pre-Qualification vs. Pre-Approval

Before you even officially enter the deep end of the loan approval process, you’ll likely encounter the “Pre-Qual” stage. I like to think of this as the “first date” of lending. You give the bank some basic info, they do a soft credit pull, and they give you a ballpark figure. It’s non-binding and doesn’t hurt your credit score.

However, if you’re serious about moving forward, you need a pre-approval. This is where the bank actually verifies your income and runs a hard credit check. In the competitive housing market of 2026, having this documented early in the loan approval process is the only way to be taken seriously by sellers. It shows you’ve already cleared the first major hurdle and that a lender has given you a preliminary “green light.”

The Core Engine: Credit Scores and History

Your credit score is the undisputed heavyweight champion of the loan approval process. When a lender pings your profile at Experian or Equifax, they are looking for a history of reliability. In my mild opinion, your score is less about how much money you have and more about how much respect you have for your obligations.

- Payment History: Have you been late in the last 24 months? This is the biggest red flag.

- Credit Utilization: Are your cards maxed out? Lenders want to see you using less than 30% of your available limit.

- Credit Mix: Do you have a healthy blend of revolving credit (cards) and installment loans (auto, student)?

If your score is looking a bit bruised, it might be worth pausing the loan approval process for a few months to polish it up. A jump of just 20 points can save you tens of thousands of dollars in interest over the life of a mortgage. You can find a deeper dive into the technicalities of scoring models on Wikipedia’s Credit Score page.

Income Verification: Proving the Paper Trail

Once the bank likes your score, they need to see the “color of your money.” For traditional W-2 employees, this part of the loan approval process is straightforward—a few paystubs and your last two years of tax returns usually do the trick. But for the growing army of freelancers and gig workers in 2026, it gets a bit more “creative.”

Lenders are now utilizing “permissioned data,” where you give them digital access to your bank statements to verify deposits in real-time. This has significantly sped up the loan approval process for self-employed individuals. They are looking for stability and “durable” income. If your earnings fluctuate wildly month-to-month, be prepared to provide a larger “buffer” of savings to prove you can handle the payments during the lean months.

The Debt-to-Income (DTI) Ratio: The Silent Decider

You could make a million dollars a year, but if you spend $950,000 of it on existing debts, you’re a high-risk borrower. This is the DTI ratio, and it is the most critical calculation in the loan approval process. Most lenders want to see your total monthly debt payments (including the new loan) stay below 36% to 43% of your gross monthly income.

If you’re hovering near the limit, the bank might ask you to pay off a small car loan or a credit card to clear some “space” in your budget. This is a common point of friction in the loan approval process, but it’s actually a safety feature. The bank doesn’t want to set you up for failure, and a lower DTI gives you the breathing room to handle life’s inevitable surprises.

Underwriting: Where the Magic (and Stress) Happens

This is the phase of the loan approval process that feels the most like a black box. Your file is handed off to an underwriter—the final judge and jury of your application. Their job is to look for the “gotchas.” They’ll double-check your employment, verify your down payment funds, and ensure the collateral (like the house or car) is actually worth the loan amount.

In 2026, many banks use automated underwriting systems for simple personal loans, which is why you can sometimes get an loan approval process completed in under ten minutes. However, for complex real estate or business deals, a human eye is still required. This is often where “conditions” come from—the underwriter might ask for a letter explaining a large deposit or proof that a past collection was settled. Don’t take it personally; it’s just them checking the boxes.

The Appraisal and Collateral Check

If the loan is “secured”—meaning it’s backed by an asset—the loan approval process includes a professional valuation. For a home, an appraiser will visit the property to ensure the price you’re paying matches the market reality. If the appraisal comes in low, it can throw a massive wrench in the loan approval process.

You then have to either negotiate the price down, cover the gap with more cash, or walk away. This step protects the lender from being “upside down” on the loan if they ever have to foreclose. It’s a vital, if sometimes frustrating, part of the risk management strategy that keeps the lending market stable. For official guidelines on these valuations, the Consumer Financial Protection Bureau offers excellent resources for borrowers.

Common “Red Flags” That Stall Progress

I’ve seen perfectly good deals fall apart late in the loan approval process because of simple mistakes. If you want to keep the momentum going, avoid these at all costs:

- Opening New Credit: Don’t apply for a new furniture store card while your mortgage is in the loan approval process. It changes your DTI and triggers a re-evaluation.

- Large Unexplained Deposits: If your Aunt Jane gives you $10,000 for your down payment, the bank needs a “gift letter” to prove it’s not another hidden loan.

- Changing Jobs: Stability is king. If you quit your job to start a business in the middle of the loan approval process, the bank will likely pull the plug.

Consistency is your best friend. From the day you apply until the day the funds are in your account, your financial life should be as boring and predictable as possible.

The Final Approval and “Clear to Close”

The three sweetest words in the English language (at least for a borrower) are “Clear to Close.” This means the underwriter has reviewed all your conditions, the appraisal is in, and the bank is ready to wire the money. At this point, the heavy lifting of the loan approval process is over.

You’ll receive a “Closing Disclosure” at least three days before you sign the final papers. Read this carefully! It lists your final interest rate, monthly payment, and exactly how much cash you need to bring to the table. This is your last chance to catch any errors before the loan approval process officially concludes and the contract becomes binding.

Closing and Funding: The Finish Line

The final step of the loan approval process is the signing ceremony. You’ll sign more papers than you ever thought possible, but once the notary is finished and the lender does a final “quality control” check, the funds are released. For a personal loan, this might be an instant wire; for a house, it might take a few hours for the county to record the deed.

It’s a moment of immense relief. You’ve successfully navigated the loan approval process, proven your worth to the financial system, and secured the capital you need to move forward. Take a second to celebrate—you’ve earned it.

FAQ Section

1. How long does the loan approval process usually take? For personal loans, it can be as fast as 24 hours. For mortgages, the average loan approval process takes between 30 and 45 days. The more organized your paperwork is, the faster it goes.

2. Can I get a loan if I’m self-employed? Absolutely. The loan approval process just requires more documentation, such as 1099s and profit-and-loss statements. Lenders in 2026 are much more comfortable with “non-traditional” income than they were a decade ago.

3. Does every loan require a hard credit pull? Usually, yes. While pre-qualification uses a “soft pull,” the official loan approval process almost always requires a hard inquiry to verify your creditworthiness.

4. What happens if my loan is denied? The lender is legally required to send you an “Adverse Action Notice” explaining why. Use this as a roadmap. If it was due to a low score, work on your credit and re-enter the loan approval process in six months.

5. What is “Private Mortgage Insurance” (PMI)? If your down payment is less than 20%, the loan approval process will include PMI. This is a monthly fee that protects the lender in case you default. It’s an extra cost, but it allows you to buy a home with much less cash upfront.

6. Can I negotiate the fees during the loan approval process? Yes! Things like “origination fees” or “application fees” are often negotiable, especially if you have a high credit score or a long history with the bank. Never be afraid to ask for a better deal.

Conclusion

At the end of the day, the loan approval process isn’t an interrogation; it’s a verification. The bank wants to lend you money—that’s how they make their profit—they just need to be sure they’re making a smart bet. By being proactive with your documentation, keeping your credit clean, and understanding the “why” behind their questions, you can navigate the system with total confidence.