Life happens fast. If you’re facing an urgent expense, learn how to secure an emergency loan in 2026, compare interest rates, and avoid predatory lending traps.

Table of Contents

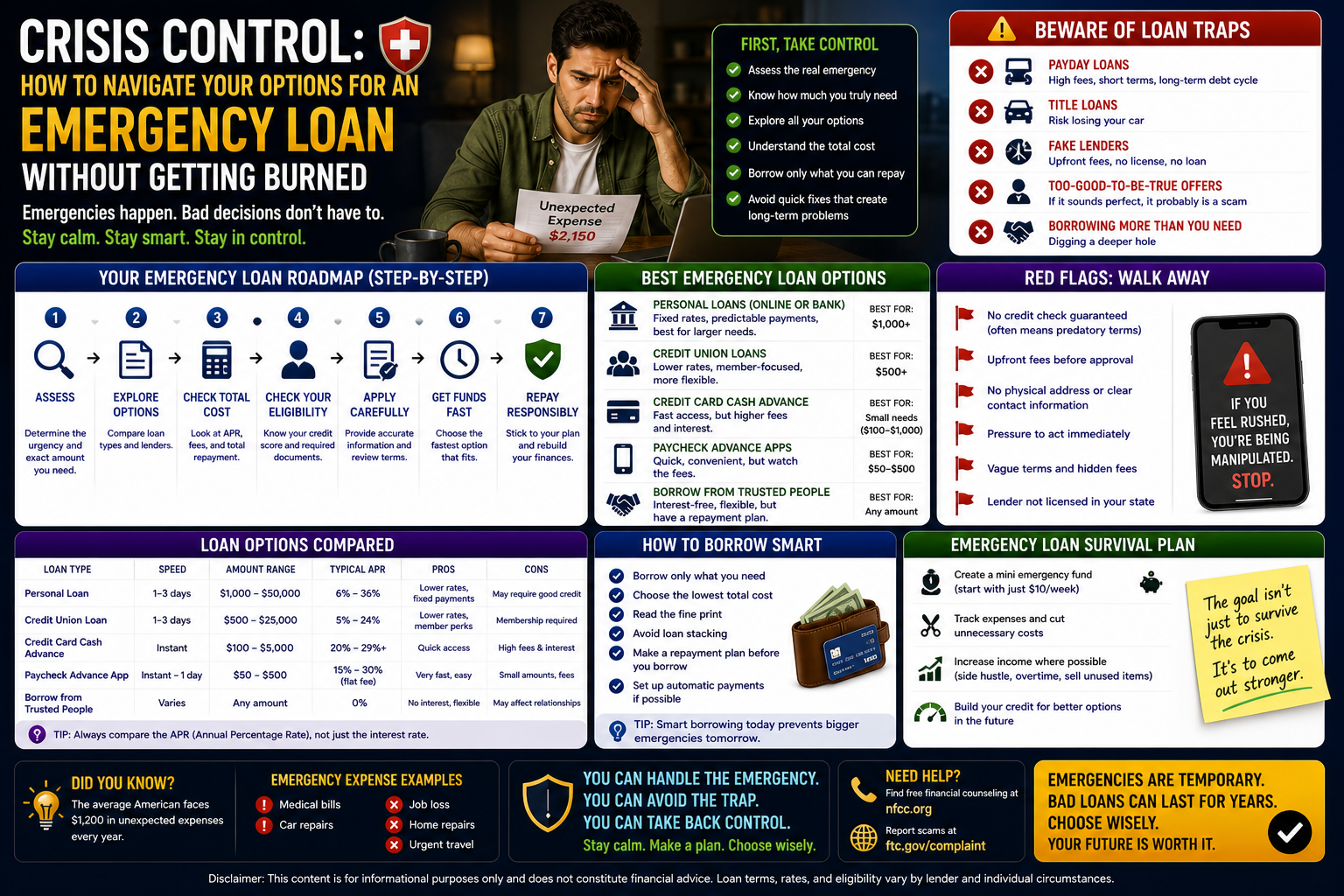

Life has a funny way of ignoring your carefully planned monthly budget. One minute you’re enjoying a quiet Tuesday evening, and the next, your water heater has decided to turn your basement into a swimming pool, or your car is making a noise that sounds suspiciously like a four-figure repair bill. We’ve all been there—that sinking feeling in the pit of your stomach when you realize you’re facing an expense that your “rainy day” fund isn’t quite ready to cover. In these high-stress moments, the search for an emergency loan becomes a frantic race against time.

However, when you’re in a rush, it’s incredibly easy to make a financial decision that solves today’s problem but creates a nightmare for next year. The lending landscape in 2026 is a crowded digital marketplace filled with everything from helpful credit unions to predatory payday lenders. Navigating this world requires a cool head, even when your basement is flooding. Securing a reliable emergency loan isn’t just about getting the cash fast; it’s about ensuring that the cost of that speed doesn’t spiral out of control.

Assessing the True Urgency of Your Situation

Before you hit “apply” on the first digital ad you see, take a deep breath. Not every financial hiccup requires a formal emergency loan. I always tell people to first ask: “Is this a ‘need it today’ or a ‘need it by next Friday’ situation?” If you have even a week of breathing room, your options expand significantly, and the interest rates you’ll pay will likely drop.

If it truly is a “need it today” crisis—like an immediate medical co-pay or a broken furnace in the dead of winter—then an emergency loan is a legitimate tool. But if you can negotiate a payment plan with the hospital or the mechanic, you might avoid taking on debt altogether. Lenders can sense desperation, and in the world of finance, desperation is expensive.

The Different Paths to Quick Funding

In 2026, the traditional bank branch on Main Street isn’t your only option. Depending on your credit score and how quickly you need the funds, there are several ways to structure an emergency loan.

- Personal Installment Loans: These are often the gold standard. You get a lump sum and pay it back in fixed monthly bites over a year or two.

- Credit Card Cash Advances: Fast, but notoriously expensive due to high interest rates and immediate fee tagging.

- Credit Union “PALs”: Many credit unions offer Payday Alternative Loans specifically designed to be a fairer version of an emergency loan for their members.

I’m a big fan of checking with local credit unions first. Because they are member-owned, they often have much more human-centric terms for an emergency loan than a massive national bank or a faceless fintech app.

How to Get Approved When Time is of the Essence

The “instant” in “instant approval” is driven by data. To get an emergency loan greenlit in minutes, you need to have your digital paperwork in order. Most modern lenders in 2026 use automated systems to verify your identity and income.

- Income Verification: Be ready to connect your bank account via a secure portal like Plaid. This allows the lender to see your pay stubs and deposit history instantly.

- Credit Score: Even for an emergency loan, your FICO score matters. While “no credit check” loans exist, they are often the most predatory.

- Debt-to-Income Ratio: Lenders want to see that you have enough room in your budget to actually pay the money back.

If your credit is less than perfect, don’t lose hope. There are specialized lenders who look at “alternative data”—like your history of paying utility bills or rent—to approve an emergency loan. For a deeper look at how these credit models have evolved, Wikipedia’s entry on Credit Scoring offers a great historical perspective.

The Hidden Costs: APR vs. Interest Rate

This is where many borrowers get tripped up in the heat of a crisis. A lender might shout about a “10% Interest Rate,” but the Annual Percentage Rate (APR) might be 25%. Why the gap? Origination fees. When you’re looking for an emergency loan, always, always look at the APR.

The APR is the “real” cost because it includes the interest plus any fees the lender takes right off the top. If you take an emergency loan for $2,000 and they charge a $100 origination fee, you only get $1,900 in your pocket but you’re paying interest on the full $2,000. It’s a subtle distinction that can cost you hundreds of dollars over the life of the loan. According to the Consumer Financial Protection Bureau, transparency in these fees is a major focus for consumer rights in 2026.

Avoiding the Payday Loan Trap

It is incredibly tempting to walk into a “fast cash” storefront when you’re stressed. They promise an emergency loan with no questions asked. But these are often the “black holes” of finance. With APRs that can reach 400%, a $500 loan can quickly turn into a $2,000 debt that you can’t escape.

If you find yourself reaching for a payday-style emergency loan, stop and look for “Salary Advance” apps or community non-profits first. Many employers now offer programs that let you access your earned wages before payday for a tiny fee or even for free. This functions as a built-in emergency loan without the soul-crushing interest rates.

Using a Co-signer to Unlock Better Rates

If your own financial history is a bit of a work-in-progress, you might need a “wingman.” A co-signer with a strong credit score can help you secure an emergency loan at a fraction of the interest rate you’d get on your own.

However, this is a serious social contract. If you miss a payment on your emergency loan, your co-signer’s credit takes the hit too. I only recommend this if you have a rock-solid plan to pay the money back. It’s an effective way to lower the cost of borrowing, but it puts a lot of trust on the line.

The Role of Fintech in 2026 Lending

The year 2026 has seen a massive surge in “Neo-banks” and specialized lending apps. These platforms have streamlined the emergency loan process to the point where you can apply on your phone while waiting for the tow truck.

Many of these apps use algorithms to provide an emergency loan based on your “future earning potential” rather than just your past mistakes. It’s a more holistic way of looking at a borrower. Just make sure the app you’re using has a valid SSL certificate and plenty of legitimate, third-party reviews. In the rush for a “fast” emergency loan, don’t sacrifice your data security.

Repayment Strategies: Getting Back to Neutral

Once the crisis is handled and the funds from your emergency loan have been spent, the “hangover” begins. The best way to manage this is to set up autopay immediately. Most lenders will actually give you a small interest rate discount (usually 0.25%) if you sign up for automatic withdrawals.

If you get a tax refund or a bonus at work, throw it at the principal of your emergency loan. Most reputable lenders in 2026 do not charge “prepayment penalties.” The faster you pay it off, the less interest you pay, and the sooner you can get back to building that elusive savings cushion.

FAQ Section

1. How fast can I actually get an emergency loan? In 2026, many online lenders can approve you in minutes and have the funds in your bank account via “Instant Transfer” within a few hours. However, a traditional bank might still take 2 to 3 business days to finalize an emergency loan.

2. What is the minimum credit score required? While it varies, a score of 600 or higher will give you access to most mainstream emergency loan options. If your score is lower, you may need to look at “secured” options where you put up collateral, like a car title.

3. Will an emergency loan hurt my credit score? Applying will trigger a “hard pull,” which might drop your score by 5-10 points temporarily. However, making on-time payments on your emergency loan will ultimately help build a stronger credit history.

4. Are there “no-interest” emergency loans? Generally, no. However, some non-profit organizations and certain employer-sponsored programs offer a emergency loan at 0% interest for employees in genuine crisis. It’s always worth checking your employee handbook first.

5. What happens if I can’t pay back the loan on time? Communication is key. If you know you’re going to be late, call the lender before the due date. Many emergency loan providers have hardship programs that can temporarily lower your payments or pause them while you get back on your feet.

6. Can I have more than one emergency loan at a time? Technically yes, but it’s a dangerous path. Taking out a second emergency loan to pay off the first one is the start of a debt spiral. It’s almost always better to talk to your original lender about a loan modification.

Conclusion

At the end of the day, an emergency loan is a tool—nothing more, nothing less. It’s like a fire extinguisher: you hope you never have to use it, but you’re incredibly glad it’s there when things start to smoke. The key to successful borrowing is to stay informed, move quickly but carefully, and always keep your eye on the “Total Cost of Capital.”