Navigating the complex world of coverage? Discover the most essential types of insurance in 2026 to protect your health, home, car, and family from the unexpected.

Table of Contents

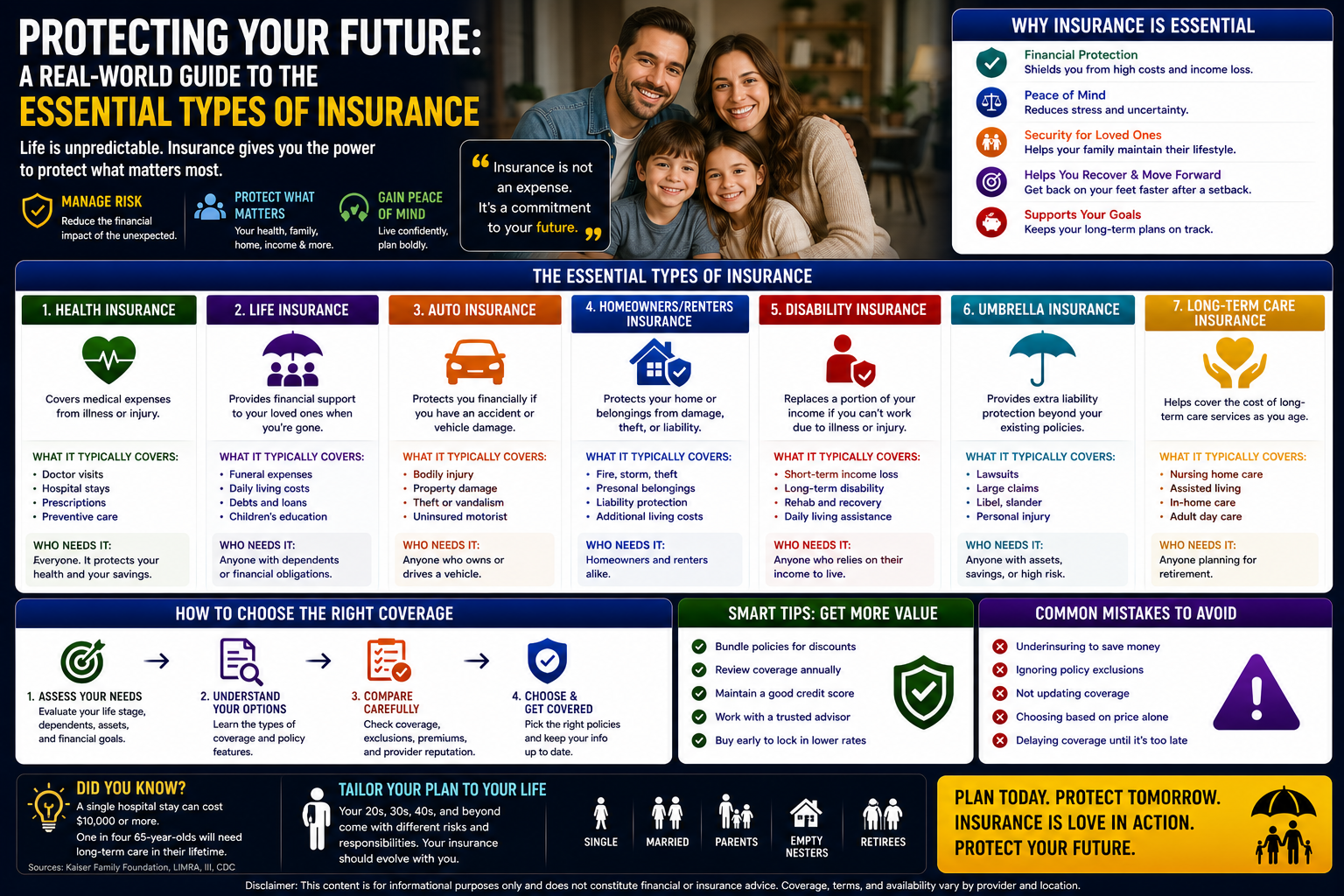

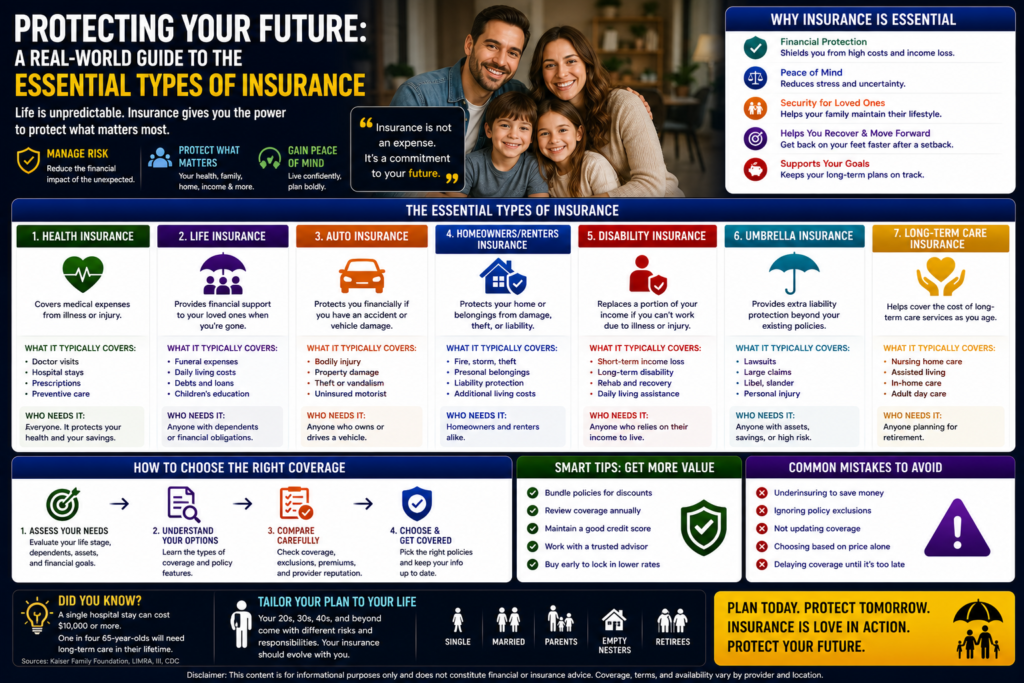

We’ve all been there—staring at a pile of paperwork or a digital dashboard, wondering why life feels like one giant subscription service for things we hope we never actually have to use. Between the monthly premiums and the confusing jargon, it’s easy to feel a bit cynical about the industry. However, the moment life throws a curveball, whether it’s a fender bender on a rainy Tuesday or a sudden health scare, that cynicism evaporates. Suddenly, having a solid understanding of the various types of insurance becomes the only thing standing between you and a financial disaster.

The reality of 2026 is that risk hasn’t gone away; it has just changed shape. We’re dealing with more expensive vehicle repairs, a shifting climate impacting our homes, and a healthcare system that remains notoriously difficult to navigate. Insurance, at its core, is just a way of pooling that risk so that one bad day doesn’t wipe out years of hard work. But you shouldn’t just buy every policy pushed your way. The goal is to build a “protection stack” that fits your actual life. Let’s break down the fundamental types of insurance you need to know about to keep your bank account—and your sanity—intact.

The Foundation: Health Insurance

If you don’t have your health, nothing else really matters, and in 2026, medical bills remain the leading cause of bankruptcy in many parts of the world. This is arguably the most critical of all the types of insurance you will ever hold. A single overnight hospital stay can cost more than a luxury SUV. Without a plan, you aren’t just risking your well-being; you’re gambling with your entire financial future.

When you’re looking at health plans, don’t just hunt for the lowest premium. You need to look at the deductible, the out-of-pocket maximum, and the network of doctors. If your favorite specialist isn’t on the list, that “cheap” plan might end up being incredibly expensive. In my experience, the types of insurance that focus on preventative care—like regular check-ups and screenings—are the ones that save you the most money in the long run. According to the World Health Organization, access to quality care without financial hardship is a global priority, and your policy is your personal gateway to that security.

Protecting Your Mobility: Auto Insurance

For most of us, our cars are our lifelines. They get us to work, pick up the kids, and facilitate the weekend getaways that keep us sane. However, as vehicles become more high-tech with sensors and cameras, even a minor “parking lot incident” can cost thousands. This is why auto coverage is one of the most common types of insurance mandated by law.

- Liability: Covers damage you cause to others.

- Collision: Repairs your own car after an accident.

- Comprehensive: Covers “Acts of God” like theft, fire, or hail.

If you’re driving an older car that’s paid off, you might consider “Liability Only” to save money. But if you’re leasing or financing a new EV, you’ll need the full suite. When comparing these types of insurance, I always suggest looking at the “uninsured motorist” coverage. It’s a small extra cost that protects you if you’re hit by someone who decided to skip their own premiums. For a deeper look at the legalities, Wikipedia’s entry on Vehicle Insurance offers a solid high-level overview.

Homeowners and Renters Insurance: Shielding Your Sanctuary

Your home is likely your biggest asset, or at the very least, it contains everything you own. Whether you own a suburban house or rent a city apartment, property coverage is a non-negotiable part of the essential types of insurance. Homeowners insurance protects the physical structure and your belongings from fire, theft, and certain natural disasters.

One thing people often overlook is “Liability Coverage” within their home policy. If someone trips over your rug and sues you, this is the part of the plan that saves your skin. For renters, don’t skip out just because you don’t “own” the walls. Your landlord’s policy won’t pay to replace your laptop or your furniture if a pipe bursts. In the world of types of insurance, renters coverage is remarkably cheap—often less than the price of a couple of pizzas a month—making it a no-brainer for anyone not living in a dorm.

Life Insurance: The Ultimate Act of Love

Let’s have the awkward conversation. Nobody likes thinking about their own mortality, but if you have people who depend on your income, life insurance is essential. It’s not for you; it’s for them. It ensures that if the worst happens, your mortgage gets paid, your kids can go to college, and your partner isn’t left in a financial lurch.

When exploring the types of insurance for life coverage, you’ll usually choose between “Term” and “Whole Life.”

- Term Life: Covers you for a set period (like 20 years). It’s affordable and straightforward.

- Whole Life: Functions as both insurance and an investment. It’s much more expensive and complex.

My mild opinion? For most families, a high-limit Term Life policy is the best value. It provides massive protection during the years you need it most (while the kids are young and the mortgage is high) without the high fees associated with investment-style types of insurance.

Disability Insurance: Protecting Your Paycheck

Think about this: what is your most valuable asset? It isn’t your car or your house. It’s your ability to earn an income over the next twenty or thirty years. If you become sick or injured and can’t work, how do you pay for all those other types of insurance? This is where disability coverage comes in.

It essentially replaces a portion of your salary if you are unable to perform your job. Many people assume they are covered by workers’ comp, but that only applies if you’re hurt at work. If you develop a chronic illness or get injured on a weekend hike, you need a private policy. It is one of the most underrated types of insurance on the market today, yet it’s the one that protects the “engine” of your entire financial life.

Navigating the Specialized “Add-Ons”

As we move through 2026, we’re seeing a surge in specialized types of insurance. These are designed to cover the gaps that traditional policies miss.

- Pet Insurance: With vet bills skyrocketing, this has become a favorite for “fur parents.”

- Cyber Insurance: Protects you from identity theft and digital fraud.

- Travel Insurance: A must-have for international trips to cover medical evacuations.

While you don’t need every niche policy, it’s worth auditing your lifestyle. If you travel four months a year or have a high-risk hobby, these specific types of insurance can be lifesavers. The key is to avoid “overlapping” coverage—don’t pay for the same thing twice through different providers.

Understanding the “Insurance Language”

Before you sign any contract for any of the types of insurance we’ve discussed, you have to understand the cost structure.

- Premium: What you pay every month to keep the policy active.

- Deductible: What you pay out of pocket before the insurance company kicks in.

- Policy Limit: The maximum amount the company will pay for a claim.

If you choose a higher deductible, your premium will go down. This is a great way to save money on the types of insurance you rarely use, but only if you have enough in your emergency fund to cover that deductible if a claim arises. It’s a delicate balancing act between monthly cash flow and long-term risk.

The Role of an Independent Agent

In the digital age, it’s tempting to just use a comparison website and buy the cheapest of all types of insurance you find. However, there is immense value in talking to an independent agent. Unlike a “captive” agent who only works for one big brand, an independent agent can shop around across dozens of companies.

They can often find discounts you didn’t know existed—like “affinity” discounts for your profession or “bundling” discounts for holding multiple types of insurance with the same carrier. Plus, when you actually have to file a claim, having a human being to call who knows your name can make a world of difference. According to the Insurance Information Institute, professional advice is often the key to avoiding “under-insurance,” which is a silent killer of financial plans.

FAQ Section

1. How many types of insurance do I actually need? At a minimum, most adults need health, auto (if you drive), and some form of property insurance (home or renters). If you have dependents, life insurance is a must. Disability insurance is also highly recommended for anyone who relies on their paycheck.

2. Is it better to bundle different types of insurance? Usually, yes. Most companies offer a “Multi-Policy Discount” if you have your home and auto insurance with them. It simplifies your billing and can save you 10% to 15% on your total premiums.

3. Does my credit score affect the cost of these types of insurance? In many regions, yes. Insurers often use a “Credit-Based Insurance Score” to predict risk. A higher credit score can lead to lower premiums for your auto and home policies.

4. Can I change my types of insurance at any time? Generally, yes. You can cancel a policy and switch to a new provider whenever you want. You don’t have to wait for the renewal date, though some companies might charge a small “short-rate” cancellation fee.

5. What is the “most expensive” of all types of insurance? Long-term, health insurance usually carries the highest premiums. However, “Whole Life” insurance can also have very high monthly costs because it includes an investment component.

6. Why do the prices of all types of insurance keep going up? Inflation, the rising cost of labor and parts, and an increase in the frequency of “catastrophic events” (like floods or storms) all contribute to rising premiums across the board.

Conclusion

At the end of the day, insurance is about peace of mind. It’s about being able to sleep at night knowing that you have a plan for the “what ifs.” Navigating the various types of insurance doesn’t have to be a headache if you take it one step at a time. Start with the essentials, audit your coverage every year, and don’t be afraid to ask questions.