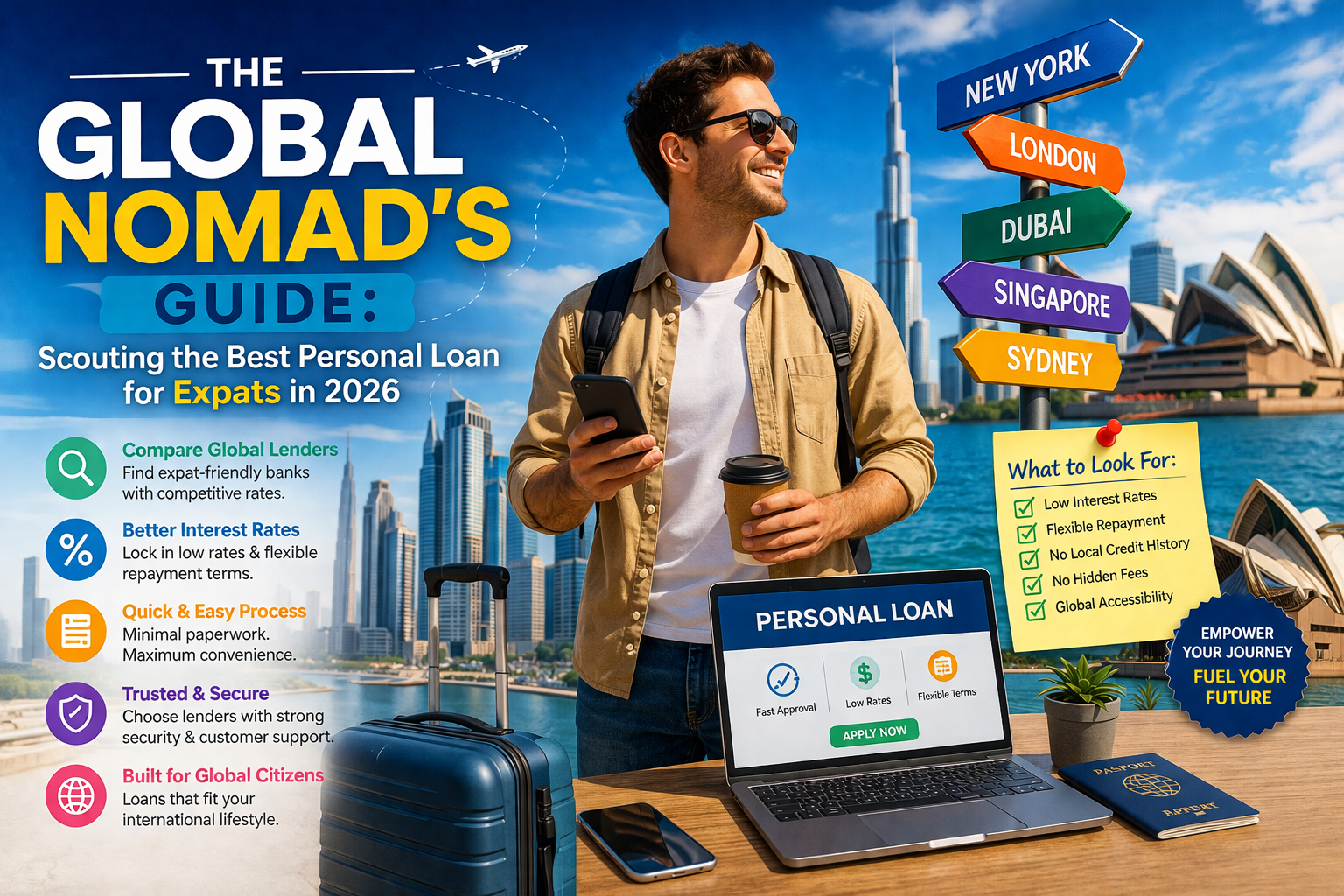

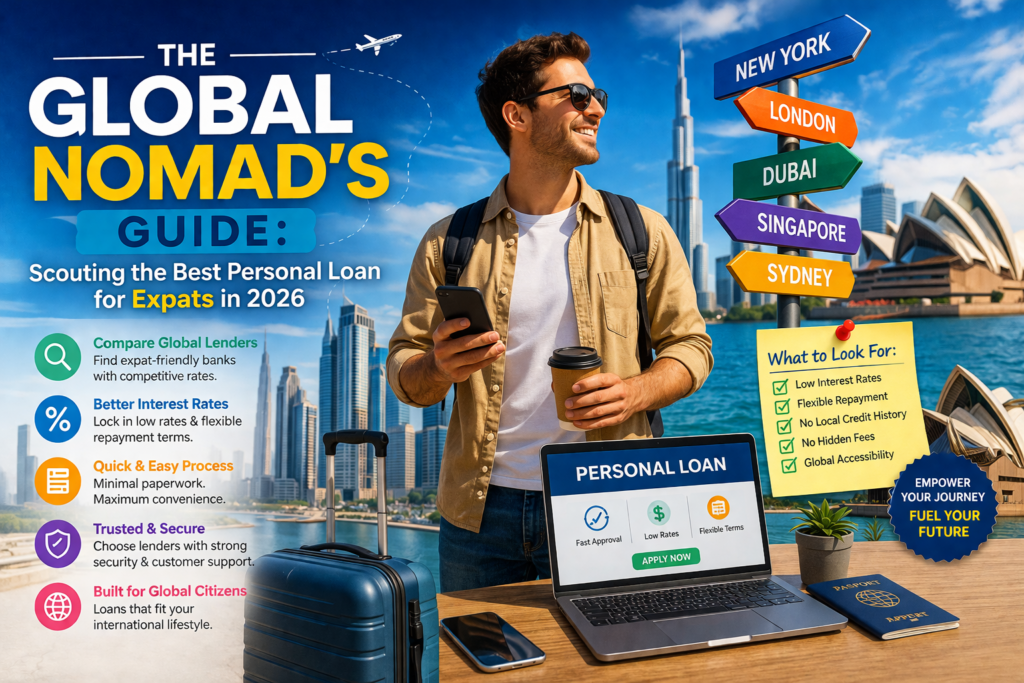

Navigating credit abroad is tough. Our expert guide helps you find the best personal loan for expats, covering interest rates, eligibility, and hidden fees.

Table of Contents

Moving to a new country is an adrenaline rush like no other. You’ve got the new job, the chic apartment in a bustling district, and a whole new culture to explore. But then, reality hits. Maybe you need to furnish that empty flat, or perhaps an unexpected medical bill pops up before your local insurance fully kicks in. Suddenly, you’re looking into borrowing money, and you realize that your stellar credit score back home doesn’t mean much to the bank down the street.

Finding the best personal loan for expats often feels like trying to solve a puzzle where the pieces are in different languages. Banks can be wary of lending to someone whose residency might be tied to a work visa. I’ve seen countless people get frustrated by the endless paperwork and the seemingly arbitrary rejections. But don’t let that discourage you. With the right strategy, securing a loan as an international resident is entirely possible. It’s all about knowing which lenders value your global profile and how to present yourself as a low-risk borrower.

Why Credit is Different When You Cross Borders

The biggest hurdle most of us face is the lack of a local credit history. You could have been a financial saint in London or New York, but in Dubai, Singapore, or Berlin, you’re starting from zero. Local banks typically rely on domestic credit bureaus to assess risk. When they pull a blank report, they get nervous.

That’s why the best personal loan for expats isn’t always found at the biggest local bank. Sometimes, international banks with a global presence are a better bet because they can occasionally look at your “cross-border” financial history. They understand that a high-earning professional on a five-year contract is a solid bet, even if they only landed three months ago. Understanding the mechanics of credit scores can help you see why local lenders are so hesitant.

What Makes a Loan “The Best” for an Expat?

When we talk about the best personal loan for expats, we aren’t just looking at the lowest interest rate. While the annual percentage rate (APR) is huge, there are other factors that can make or break the deal for someone living abroad.

- Speed of Approval: If you need bond money for a rental, you can’t wait six weeks.

- Flexibility: Can you pay the loan off early if you decide to move to a different country?

- Repatriation Terms: What happens to the loan if your visa isn’t renewed?

- Digital-First Experience: As an expat, you’re likely tech-savvy. You want an app, not a physical branch.

I’ve found that the best personal loan for expats usually comes from a lender that offers a “no-early-exit-fee” clause. Life abroad is unpredictable. If you get a surprise promotion that moves you to Tokyo, you don’t want to be penalized for settling your debts in Madrid before you leave.

Criteria for Finding the Best Personal Loan for Expats

So, how do you actually separate the wheat from the chaff? You have to look at the eligibility requirements. Most lenders will ask for a minimum salary, a valid residency permit, and a local bank account that has been active for at least three to six months.

To snag the best personal loan for expats, you should aim to have your paperwork in perfect order. This usually includes your employment contract, several months of pay slips, and a letter from your employer confirming your “end-of-service” benefits or salary transfer. Lenders love stability. If you can show that you work for a reputable multinational or a well-known local firm, you’re already halfway there.

Interest Rates and Hidden Fees

Let’s talk money. Interest rates for expats are often slightly higher than for locals. It’s a “risk premium.” However, the best personal loan for expats should still be competitive. Watch out for processing fees, which can range from 1% to 3% of the total loan amount.

Also, keep an eye on life insurance requirements. Many regions require you to take out a policy that covers the loan amount in case of an accident. While it adds a few dollars to your monthly payment, it actually makes you a more attractive candidate for the best personal loan for expats because it guarantees the bank gets their money back regardless of what happens.

Regional Variations: Where You Live Matters

Your location changes the game entirely. In the Middle East, for instance, salary transfer loans are the norm. This is often where you find the best personal loan for expats because the bank has direct access to your monthly income, which lowers their risk and, consequently, your interest rate.

In Europe, the focus might be more on your long-term residency prospects. If you have an EU Blue Card, you’ll find it much easier to access the best personal loan for expats compared to someone on a short-term visitor-to-work conversion. Each market has its quirks, and International Monetary Fund reports often highlight how different banking regulations affect consumer lending in these emerging and developed hubs.

The Role of Digital and Neobanks

We can’t ignore the rise of digital-only banks. For many, these represent the best personal loan for expats because they were built for the modern, mobile workforce. These lenders often use alternative data to verify your income and identity.

They might look at your utility bill payments, your rent history, or even your professional LinkedIn profile to build a risk model. If you’re struggling with a traditional high-street bank, a fintech challenger might offer the best personal loan for expats simply because they are more comfortable with non-traditional credit footprints.

Tips to Improve Your Approval Odds

If you’ve been rejected once, don’t panic. There are several things you can do to make yourself the ideal candidate for the best personal loan for expats next time around.

- Lower Your Debt-to-Income Ratio: Pay down your credit cards before applying.

- Stay Put: Lenders hate seeing three different home addresses in six months.

- Build Local History: Even if you don’t need a loan yet, get a local credit card and pay it off in full every month.

- Show Your Assets: If you have investments back home, show the bank. It proves you have a safety net.

Securing the best personal loan for expats is often about building a narrative of responsibility. Show them you aren’t just passing through, but that you are an active, contributing member of the local economy.

Red Flags to Avoid

In your search for the best personal loan for expats, you might stumble upon some “too good to be true” offers. Avoid any lender that asks for an “upfront fee” before the loan is approved—this is a classic scam.

Also, be wary of predatory lenders who target foreigners with sky-high interest rates. The best personal loan for expats will always be transparent. If the contract is hundreds of pages of fine print that the agent can’t explain, walk away. Your financial health is worth more than a quick cash injection.

Negotiating the Terms

Most people don’t realize that you can actually negotiate with banks. If you have a high salary and a solid contract, you can push for a better rate. Tell them you’re looking for the best personal loan for expats and that you’re comparing their offer with a rival bank.

Sometimes, the bank will waive the processing fee or shave half a percent off the interest rate just to get your business. Remember, you are a valuable customer. Expats often bring high deposits and foreign exchange business to banks, so use that as leverage when hunting for the best personal loan for expats.

FAQ Section

1. Can I get a personal loan if I just moved to the country? It’s tough but possible. Most lenders want to see at least three months of local salary history. However, some specialized lenders offer the best personal loan for expats specifically for newcomers who have a confirmed contract from a top-tier employer.

2. Does my credit score from my home country count? Usually, no. Most credit systems are national. However, some international banks (like HSBC or Citibank) might look at your global history to help you secure the best personal loan for expats in a new market.

3. What is the maximum amount I can borrow? This usually depends on your monthly salary. In many countries, your total monthly debt payments (including the new loan) cannot exceed 50% of your income. This regulation ensures that even with the best personal loan for expats, you still have enough money to live on.

4. What happens if I lose my job? This is a critical question. Most loans for expats include mandatory credit insurance. If you lose your job due to redundancy, the insurance might cover your payments for a few months while you look for a new role. Always check this before signing for what you think is the best personal loan for expats.

5. Are digital banks safe for personal loans? Yes, provided they are fully licensed in the country where they operate. Many people find the best personal loan for expats through these platforms because of their lower overhead costs and faster processing times.

6. Can I use a personal loan for a down payment on a house? Technically, yes, but be careful. Taking out a personal loan increases your debt-to-income ratio, which might make it harder to get a mortgage later. The best personal loan for expats should be used for manageable expenses, not as a way to over-leverage yourself.

Conclusion

Living as an expat is an incredible adventure, but the financial hurdles can be a real buzzkill. Finding the best personal loan for expats requires a mix of patience, thorough documentation, and a bit of local know-how. Don’t settle for the first offer that comes your way. Shop around, compare the APRs, and look closely at the fine print.