Maximize every dollar. Discover the best credit cards for cashback in 2026, from grocery-focused rewards to flat-rate winners, and start earning today.

Let’s be honest: who doesn’t like free money? In the current economic climate, where every trip to the grocery store or gas station seems to cost a little more than it did last month, getting a percentage of that spend back in your pocket isn’t just a perk—it’s a survival strategy. If you’re still using a debit card or a basic credit card that doesn’t reward you, you’re essentially leaving a “cashback tax” on the table. Finding the best credit cards for cashback is one of the easiest ways to give yourself a passive raise without ever having to ask your boss for a cent.

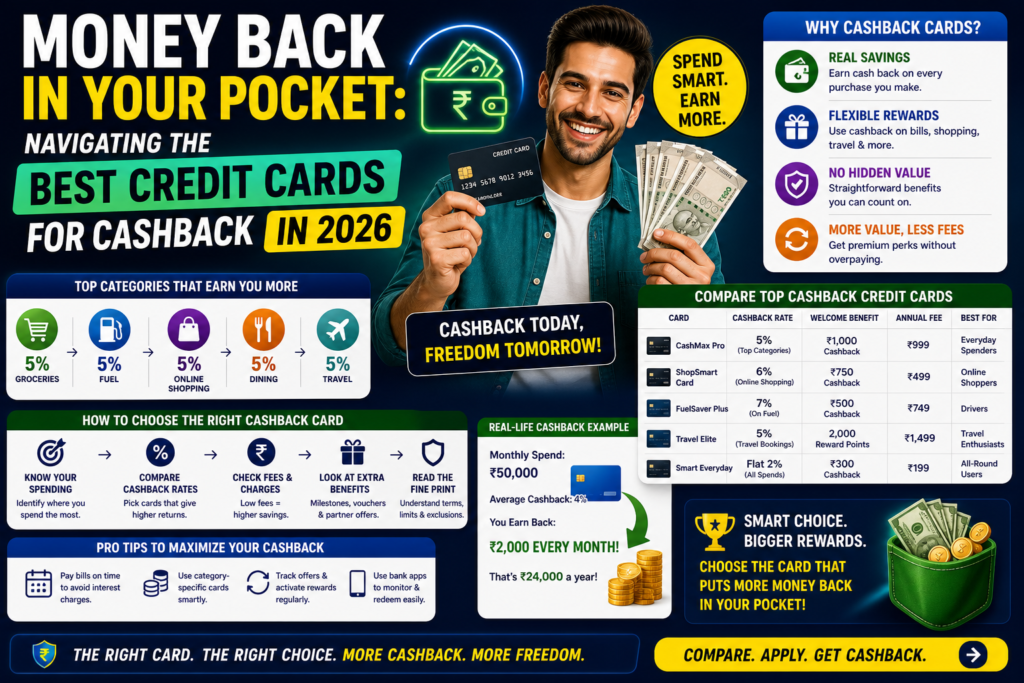

But here is the catch: the “best” card for me might be a total dud for you. I’ve seen people obsess over a 6% grocery reward card only to realize they spend most of their money on dining out. Choosing from the best credit cards for cashback is a highly personal decision that depends entirely on your specific lifestyle and spending habits. In 2026, the market is more competitive than ever, with issuers fighting for your loyalty through massive welcome bonuses and niche categories like streaming services or transit. Let’s break down how to filter through the noise and find your perfect match.

The Big Divide: Flat-Rate vs. Tiered Rewards

When you start your search for the best credit cards for cashback, you’ll notice two main architectures.

- Flat-Rate Cards: These are the “set it and forget it” champions. They offer a steady percentage—usually 2% in 2026—on every single purchase, regardless of what it is.

- Tiered/Category Cards: These offer higher percentages (like 3% to 6%) on specific categories like gas, groceries, or dining, but only 1% on everything else.

I’m a firm believer that for most people, the best credit cards for cashback strategy actually involves a “duo.” Use a high-tier category card for your big expenses like food and fuel, and then switch to a flat-rate card for everything else. It takes a little more effort to remember which card to pull out at which store, but the difference in your annual earnings can be hundreds of dollars.

Best for Groceries and Everyday Essentials

If you have a family, your biggest monthly expense—aside from the mortgage—is likely the supermarket. In 2026, the best credit cards for cashback for groceries often feature rates as high as 6%.

The Blue Cash Preferred® Card from American Express continues to be a heavyweight in this category, offering a massive 6% back at U.S. supermarkets (up to $6,000 per year). If you hit that cap, that’s $360 back just for buying milk and bread. However, keep an eye on annual fees. Often, the best credit cards for cashback with the highest tiers come with a yearly charge. You have to do the math: if the fee is $95 but you’re earning $400 in rewards, you’re still $305 ahead. For those who prefer a $0 fee, the SavorOne Rewards from Capital One is a fantastic alternative, offering a solid 3% on dining, entertainment, and groceries.

The Power of the Flat-Rate Winner

For those of us who don’t want to play the “which category is this?” game, the best credit cards for cashback are the ones that keep it simple. The Wells Fargo Active Cash® Card has become a staple for its unlimited 2% cash rewards on all purchases.

Why is this so powerful? Because life is full of “miscellaneous” expenses. Repairs at the mechanic, new shoes for the kids, or that random Target run usually fall into the 1% bucket on most cards. By using one of the best credit cards for cashback that offers a flat 2%, you’re doubling your earnings on the vast majority of your life’s “un-categorized” spend. It provides a level of financial predictability that is hard to beat.

Maximizing Your Welcome Bonus

In 2026, credit card companies are desperate for high-quality customers. This means the sign-up offers are reaching historic highs. When looking for the best credit cards for cashback, the welcome bonus is often the “cherry on top” that can pay for a weekend getaway.

Typical offers right now involve earning $200 to $300 after spending about $500 to $1,000 in the first three months. While it’s tempting to grab every card with a big bonus, remember that “churning” can impact your credit score. The best credit cards for cashback for you should be ones you plan to keep for years, not just for the initial “free” cash. For a deeper look at the technicalities of how these offers affect your credit profile, Wikipedia’s page on Credit Cards offers a great historical perspective on the industry’s evolution.

Navigating the 0% Intro APR Period

Sometimes, the best credit cards for cashback serve a dual purpose. Many top-tier cards in 2026 come with a 0% Introductory APR on purchases for 12 to 15 months.

If you have a big purchase coming up—like a new refrigerator or a set of tires—you can earn the cashback on that purchase and pay it off interest-free over a year. It’s a savvy way to manage cash flow. However, be careful. Once that intro period ends, interest rates in 2026 are hovering around 19% to 22%. If you carry a balance past the intro window, the interest will quickly wipe out any earnings you made from the best credit cards for cashback. Always treat these cards like a debit card—only spend what you can afford to pay off.

Business Cashback: A Goldmine for Entrepreneurs

If you run a small business or even a side hustle, the best credit cards for cashback are specifically tailored to your overhead. Cards like the Ink Business Cash® Credit Card offer up to 5% back on office supplies, internet, and phone services.

For many freelancers, these categories represent their biggest recurring costs. By using one of the best credit cards for cashback for business, you can essentially get a 5% discount on your utilities every month. According to data from Forbes Advisor, business owners who optimize their credit spend often see a 2-3% increase in their net margins purely from rewards. It’s an easy win for anyone looking to professionalize their finances.

Avoiding the “Redemption” Traps

What good is cashback if you can’t actually use it? Some of the best credit cards for cashback have annoying rules about how much you need to earn before you can cash out. You might need to reach $25 or $50 before you can see that money in your bank account.

The truly best credit cards for cashback in 2026 offer “Any Amount, Any Time” redemptions. Whether you have $0.50 or $500, you should be able to apply it as a statement credit or send it to your checking account. When you are comparing cards, check the redemption terms. If you have to jump through hoops or buy gift cards just to access your rewards, it’s not really one of the best credit cards for cashback for a busy person.

The Impact of Your Credit Score

Let’s talk reality for a second: to get the absolute best credit cards for cashback, you generally need a “Good” to “Excellent” credit score (usually 670 or higher). If your score is in the 500s or low 600s, you might be limited to cards with lower reward rates or even “secured” cards.

However, don’t lose heart. Even a card with 1% back is better than 0%. Many of the best credit cards for cashback offer tools to help you monitor and grow your score. As your score climbs, you can “graduate” to the top-tier cards. It’s a journey, and every step closer to that 750+ score unlocks more of the best credit cards for cashback options with higher limits and better perks.

Digital Security and Mobile Integration

In 2026, your card should live in your digital wallet as much as your physical one. The best credit cards for cashback now offer sophisticated mobile apps that track your spending categories in real-time.

You should be able to see exactly how much “grocery” vs. “dining” spend you have at any moment. This helps you realize if you’re using the wrong card for a specific category. Furthermore, the best credit cards for cashback should have “Virtual Card” features. This allows you to generate a unique card number for online shopping, protecting your main account if a merchant gets hacked. It’s about more than just rewards; it’s about protecting your financial identity in an increasingly digital world.

FAQ Section

1. Is cashback better than travel points?

It depends on your goals. Cashback is the best credit cards for cashback choice for people who want simplicity and a guaranteed return. Travel points can be more valuable if you know how to “transfer” them to airlines, but they require much more work. If you just want to lower your monthly bills, go with cashback.

2. Do I have to pay taxes on my cashback?

Generally, no. The IRS views cashback from the best credit cards for cashback as a “rebate” on a purchase rather than income. However, if you earn a bonus just for opening an account (without a spending requirement), that might be taxable. Always check with a tax pro if you’re unsure.

3. Does applying for multiple cards hurt my credit score?

A formal application involves a “hard pull,” which might drop your score by 5 to 10 points temporarily. If you apply for three of the best credit cards for cashback in one week, it might look like you’re desperate for credit, which can be a red flag to lenders. Space out your applications by at least 3 to 6 months.

4. What is the average interest rate for cashback cards in 2026?

Currently, the average APR is around 19.16%. The best credit cards for cashback often have higher interest rates than non-reward cards. This is why it is vital to pay your balance in full every month; if you carry debt, you’ll pay far more in interest than you’ll ever earn in cashback.

5. Can I get a cashback card with no annual fee?

Absolutely. Many of the best credit cards for cashback—like the Citi Double Cash® or Wells Fargo Active Cash®—have $0 annual fees. These are perfect for people who want to earn rewards without any “overhead” costs.

6. Do cashback rewards expire?

On the best credit cards for cashback, rewards typically do not expire as long as your account remains open and in good standing. However, always check your specific card’s terms, as some store-branded cards might have different rules.

Conclusion

At the end of the day, your credit card should be a tool that works for you, not the other way around. Finding the best credit cards for cashback is a simple way to take a little bit of the sting out of inflation and make your everyday spending a little more rewarding.