Planning a getaway? Learn why insurance for international trips is your most important travel essential. Compare coverage, avoid scams, and travel with peace of mind.

Table of Contents

There is nothing quite like that feeling of hitting “confirm” on a flight to a destination you’ve been dreaming about for years. Whether it’s the cobblestone streets of Prague, the bustling night markets of Bangkok, or a quiet villa in Tuscany, the excitement is palpable. You’ve packed the right shoes, downloaded the offline maps, and converted your currency. But there is one invisible item that often gets left behind in the rush of excitement: insurance for international trips. It’s the least glamorous part of travel planning, yet it’s the only thing that can stand between a dream vacation and a financial catastrophe.

I’ve spent years traveling and writing about the industry, and if there is one thing I’ve learned, it’s that the “it won’t happen to me” mindset is a dangerous game. From a sudden ear infection in a country where you don’t speak the language to a lost suitcase containing your most expensive gear, the unexpected is the only thing you can truly count on when you cross borders. Securing proper insurance for international trips isn’t just about being “responsible”—it’s about protecting the investment you’ve made in your own happiness and relaxation.

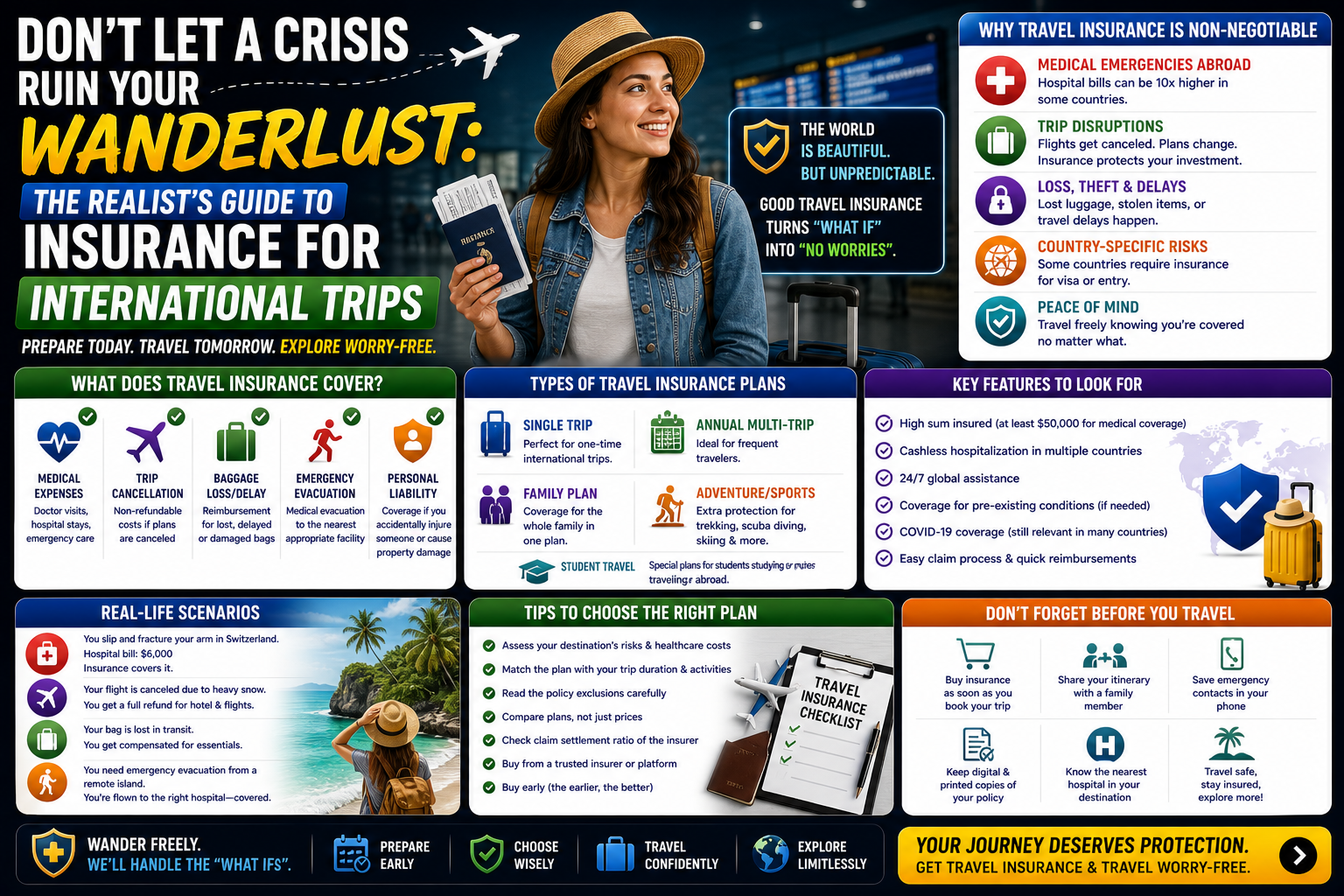

Why Your Domestic Health Plan Isn’t Enough

One of the most common myths I hear is that “my regular health insurance covers me everywhere.” For 95% of people, that is unfortunately not true. Most domestic health plans stop at the border. Even if they offer “emergency” coverage, they often require you to pay thousands of dollars upfront and fight for reimbursement months later. When you take out specialized insurance for international trips, you are essentially buying a concierge service that handles the complexity of foreign medical systems for you.

In 2026, the cost of medical care globally has skyrocketed. A simple overnight hospital stay in a private clinic in a tourist hub can easily cost more than your entire business-class flight. Having insurance for international trips ensures that a minor medical hiccup doesn’t turn into a decade of debt. It’s the difference between being treated as a priority patient and being stuck in a bureaucratic limbo while you’re already feeling your worst.

Decoding the Different Layers of Coverage

When you start shopping for insurance for international trips, it’s easy to get overwhelmed by the jargon. You aren’t just buying one “thing”; you’re buying a bundle of protections. Here is how to break it down like a pro:

- Medical Emergency & Evacuation: This is the big one. If you’re hiking in a remote area and need a helicopter, or if you need to be flown home on a medical flight, this coverage is a literal lifesaver.

- Trip Cancellation & Interruption: If a family member gets sick or your boss cancels your vacation at the last minute, this ensures you get your non-refundable deposits back.

- Baggage and Personal Effects: For those of us traveling with laptops, cameras, or designer gear, this is vital.

- Travel Delay: Stuck in an airport for 24 hours because of a strike? This covers your hotel and meals while you wait.

I always tell my readers to look for insurance for international trips that offers at least $100,000 in medical coverage and $500,000 in evacuation. It sounds like a lot, but in the world of private medical jets, that money vanishes surprisingly fast.

The 2026 “Tech-Factor”: Apps and Instant Claims

The industry has changed significantly in the last couple of years. Gone are the days of mailing physical receipts to an office in the Midwest. Today, the best providers of insurance for international trips offer integrated apps where you can video-chat with a doctor in your native language 24/7.

Some even offer “Instant Payouts” for flight delays. If the airline’s data shows your flight is delayed by more than four hours, the app automatically pings you and deposits a meal or hotel voucher directly into your digital wallet. When you compare insurance for international trips, look for these “quality of life” features. They take the sting out of a bad situation and let you get back to your holiday with minimal friction.

Navigating Pre-Existing Conditions

This is the area where people often get tripped up. If you have a chronic condition, you must be transparent when buying insurance for international trips. Many plans offer a “Pre-existing Condition Waiver” if you purchase the policy within a specific window (usually 14–21 days) of making your first trip deposit.

If you ignore this, the insurer can deny your claim if they decide your emergency was related to a past issue. It’s not worth the risk. A solid insurance for international trips policy will clearly outline what is covered and what isn’t. According to the U.S. Department of State, checking these details is the single most important step for any citizen traveling abroad.

Understanding “Cancel For Any Reason” (CFAR)

Sometimes, you just change your mind. Maybe the weather looks terrible, or you’ve just got a bad feeling about a destination. Standard insurance for international trips won’t cover you for “cold feet.” For that, you need CFAR.

It usually costs about 40% more, and it typically only pays back 50% to 75% of your costs, but it offers the ultimate flexibility. If you are a nervous traveler or if your destination is politically unstable, adding CFAR to your insurance for international trips is a brilliant way to protect your peace of mind. It’s the “eject button” that every high-stakes traveler should at least consider. For a deeper look at the legalities of these contracts, Wikipedia’s Travel Insurance page offers a great historical perspective on how these policies evolved.

External Links and Industry Standards

To truly find the best protection, you should use independent comparison tools. I recommend checking out sites like InsureMyTrip or SquareMouth, which allow you to compare dozens of providers side-by-side. They also offer verified customer reviews, which are essential for seeing how a company actually behaves when someone files a claim.

Don’t just look for the cheapest insurance for international trips. Look for the company that actually picks up the phone when you’re calling from a train station in rural Japan at 4:00 AM. That level of service is worth every extra penny.

Common Scams and How to Avoid Them

The travel space is unfortunately rife with “ghost” insurers. These are websites that look professional but offer insurance for international trips that isn’t backed by any real underwriter.

- Check the Underwriter: Every policy should be backed by a major company like AIG, Allianz, or Berkshire Hathaway.

- Verify the License: Ensure the company is licensed to sell insurance in your home state or country.

- Read the Schumer Box: Look at the table of limits and exclusions. If it’s too vague, it’s a red flag.

A legitimate insurance for international trips provider will have a clear, easy-to-read policy document. If they try to hide the exclusions in a 50-page PDF of legalese, they probably aren’t in your corner.

The Role of Credit Card Insurance

Many “Premium” credit cards (like the Amex Platinum or Chase Sapphire Reserve) offer built-in travel protection. While these are great, they are often “Secondary” coverage. This means you have to exhaust all other options before they pay out.

Using your credit card perks as a supplement to dedicated insurance for international trips is a smart move, but relying on them as your only protection is risky. They often have low caps on medical coverage and may not cover things like search and rescue or medical evacuation to your home country. For a serious adventure, dedicated insurance for international trips is non-negotiable.

FAQ Section

1. Is insurance for international trips mandatory? For some countries, yes. Destinations like Cuba, Turkey, and many Schengen Area countries require proof of medical coverage to issue a visa. Even if it’s not required, insurance for international trips is highly recommended for any trip away from home.

2. When should I buy my policy? The best time is immediately after you book your flights or hotel. This ensures you are covered for “Trip Cancellation” from day one. If you wait until the week before you leave, you might miss the window for certain benefits like pre-existing condition waivers.

3. Does insurance for international trips cover adventure sports? Usually, you need an “Adventure Sports” add-on. Standard policies often exclude things like scuba diving, bungee jumping, or skiing. If your trip involves adrenaline, make sure your insurance for international trips specifically lists those activities.

4. How much does it typically cost? Expect to pay between 4% and 10% of your total pre-paid trip cost. For a $3,000 trip, a policy for insurance for international trips will likely cost between $120 and $300, depending on your age and the coverage level.

5. Can I buy insurance for international trips if I’m already abroad? Yes, but your options will be limited. Most companies require you to be in your home country when you purchase the policy. A few specialized “nomad” insurers allow you to buy coverage while traveling, but there is usually a 48-hour waiting period before it becomes active.

6. What is a “Named Peril” policy? This is a policy that only covers very specific events listed in the contract (like a hurricane or a strike). It’s often cheaper, but it’s less comprehensive than a “Cancel For Any Reason” or a broad insurance for international trips plan.

Conclusion

At the end of the day, travel is about discovery, growth, and relaxation. It’s about stepping out of your comfort zone and into the wide, beautiful world. But the world can be unpredictable, and being prepared is what separates an adventure from a disaster. Taking the time to secure insurance for international trips isn’t just another chore on your to-do list; it’s an act of self-care.