Moving abroad? Learn how to find a loan for expats with low interest in 2026. We cover credit building, the best lenders, and expert tips to save you money.

Table of Contents

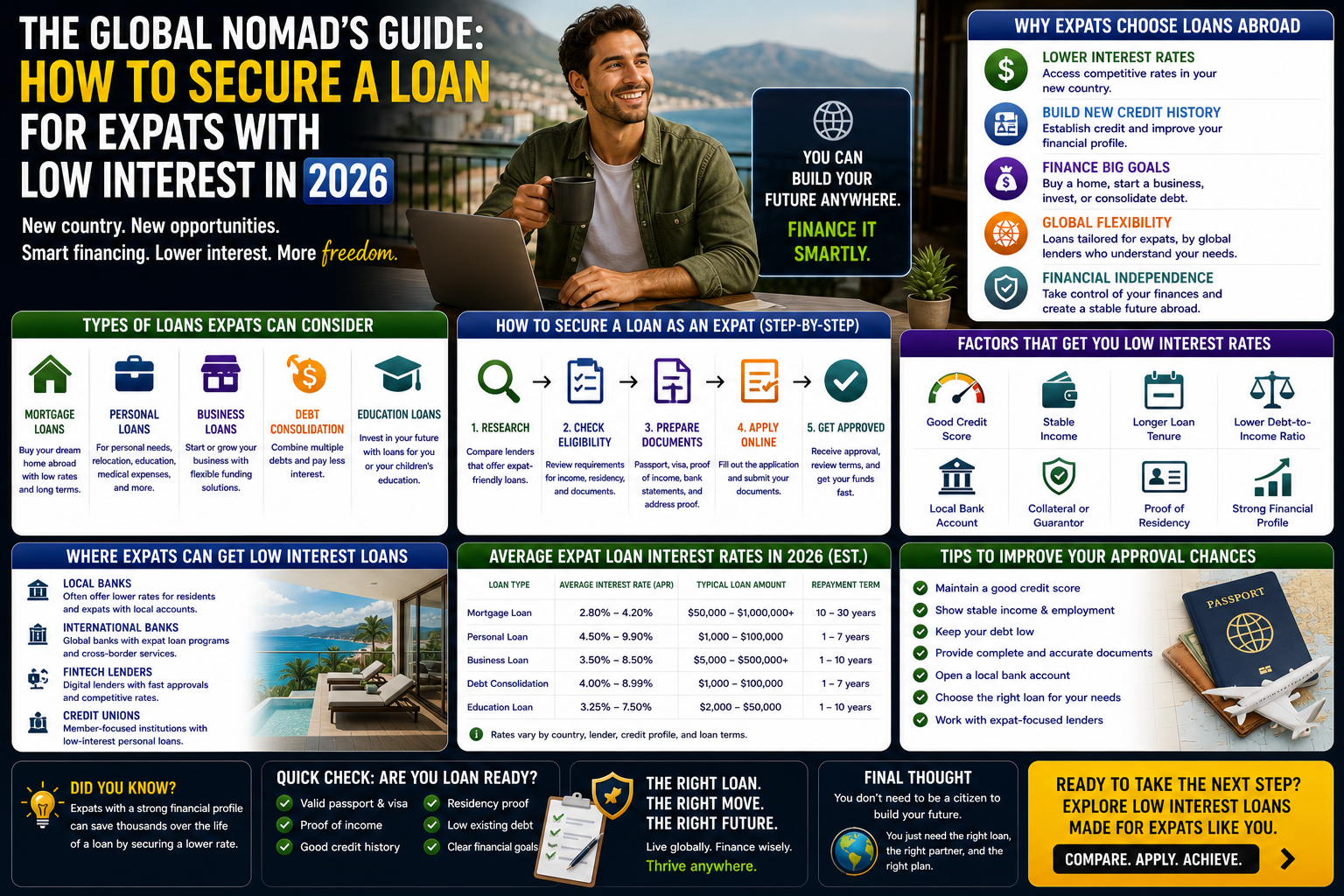

Moving your life to a new country is an exhilarating whirlwind of culture, new beginnings, and, let’s be honest, significant expenses. Between the security deposits, shipping crates, and the inevitable “I forgot I needed a car” realization, your bank account can take a serious beating. I’ve spoken to so many people who feel stuck because, despite having a great salary, they are treated like financial ghosts the moment they cross a border. Finding a loan for expats with low interest often feels like trying to find a unicorn in a busy city—it’s frustrating, overwhelming, and sometimes feels impossible.

The reality of the 2026 lending market is that banks are cautious. When they see a residency visa with an expiration date, their risk assessment software starts blinking red. But here is the good news: you don’t have to settle for predatory rates. The financial world is finally waking up to the nomadic nature of modern work. Securing a loan for expats with low interest is now more achievable than ever, provided you know which levers to pull and how to present your global profile as an asset rather than a liability.

The “Credit Reset” Reality Check

The biggest hurdle you’ll face is the “credit reset.” You might have a perfect score back home, but the moment you land in a new jurisdiction, you’re often back at square one. This lack of local history is exactly why it’s so hard to find a loan for expats with low interest in your first few months. Most local credit bureaus simply don’t talk to each other across borders, which feels incredibly unfair when you’ve spent years being fiscally responsible.

However, some international banks are starting to utilize “cross-border credit” reporting. This allows them to look at your financial behavior in your home country to justify a loan for expats with low interest right away. If you’re moving from the US to the UK, or the UK to the UAE, checking for lenders that use services like Nova Credit can be a total game-changer for your wallet.

Why Salary Transfer is Your Best Friend

If you want to command the absolute best rates, you have to be willing to play ball with the bank’s security needs. In my experience, the most reliable path to a loan for expats with low interest is through a “Salary Transfer” arrangement. This is where you agree to have your monthly paycheck deposited directly into the bank that is lending you the money.

Banks love this because it virtually eliminates their risk. They know they are the first to get paid every month before you even see the cash. This added security is your biggest point of leverage. When you offer a salary transfer, you move from the “high-risk” bucket to the “preferred” bucket, which is where those elusive loan for expats with low interest offers are hidden.

Traditional Banks vs. Fintech Challengers

In 2026, you have more options than just the big high-street names. The quest for a loan for expats with low interest now includes a variety of agile fintech companies that use “alternative data” to judge your creditworthiness.

- Traditional Banks: Offer stability and higher lending amounts but involve more bureaucracy and mountain-high paperwork.

- Fintech Lenders: Use your educational background, job title, and professional LinkedIn profile to assess you. They are often faster but might have lower maximum loan limits.

I usually suggest getting a quote from both. A digital challenger might offer you a loan for expats with low interest based on your “future earning potential,” while a traditional bank might give you a better rate if you’ve been in the country for at least six months. According to Wikipedia’s entry on Credit Scores, lenders are increasingly looking at these non-traditional data points to price risk more accurately.

Key Eligibility Criteria for International Residents

Lenders aren’t just looking at your income; they’re looking at your stability. To successfully secure a loan for expats with low interest, you generally need to satisfy three main pillars:

- Length of Residency: Most top-tier lenders want to see at least 3 to 6 months of local bank statements.

- Company Listing: Does your employer have a good reputation locally? Working for a multinational often makes getting a loan for expats with low interest much easier.

- Visa Validity: Lenders rarely offer a term that exceeds the length of your current residency permit.

By meeting these criteria, you prove that you aren’t a “flight risk.” When a bank feels confident that you’ll be in the country for the duration of the repayment, they are much more likely to offer a loan for expats with low interest.

The Role of the “Debt-to-Income” Ratio

Your Debt-to-Income (DTI) ratio is the silent decider in your application process. Even if you have a massive salary, if 40% of it is already going toward a mortgage back home or car payments, a bank won’t give you a loan for expats with low interest. They want to see that you have plenty of “breathing room” in your monthly budget.

Before applying, try to pay off any small, lingering debts. Lowering your DTI by even 5% can be the difference between a “Standard” rate and a loan for expats with low interest. It shows the lender that you are in total control of your cash flow, which is the hallmark of a low-risk borrower in any country.

Understanding APR and Hidden Fees

This is where people get tripped up. A lender might shout about a “3% Interest Rate,” but when you look at the Annual Percentage Rate (APR), it’s actually 6%. Why? Because of origination fees, processing charges, and mandatory insurance. To find a true loan for expats with low interest, you must look at the APR.

The APR is the “real” cost of the loan because it includes both the interest and the fees. A loan for expats with low interest with a slightly higher base rate but zero processing fees is often cheaper than a “low-rate” loan with a $500 admin charge buried in the fine print. Always ask for a “Total Cost of Credit” statement before you sign anything.

Strategic Timing: When to Apply

Timing is everything. I’ve seen expats apply for a loan the week they land and get rejected, only to apply three months later and get a loan for expats with low interest. Most banks want to see that you’ve passed your “probation period” at work.

Wait until you have three full months of local paystubs and a utility bill in your name. This “paper trail” proves that you are integrated into the local system. It might feel like a long wait when you’re sleeping on a borrowed mattress, but that patience is what unlocks the loan for expats with low interest that will save you thousands over the next few years.

Negotiating Your Rate

One mild opinion I hold is that everything is negotiable—even bank rates. If you have a high salary and work for a reputable firm, don’t just accept the first offer. Take your quote from a fintech lender to your main bank and ask them to beat it.

Banks are hungry for high-quality expat customers in 2026. If you can show them a competing offer, they will often “shave off” a fraction of a percent to win your business. That tiny fraction might not seem like much, but on a five-year loan for expats with low interest, it adds up to a lot of extra dinners out in your new city. You can find more data on global interest trends through the World Bank to see how your local rates compare to the global average.

Avoiding the “Expat Trap” of High-Interest Credit Cards

It’s tempting to just put your relocation costs on a new credit card and “deal with it later.” This is a massive mistake. Credit card interest rates are often double or triple what you would find with a structured loan for expats with low interest.

By taking the time to set up a proper personal loan, you give yourself a fixed end date and a much lower cost of capital. It keeps your credit utilization low and protects your long-term financial health in your new home. A loan for expats with low interest is a strategic move; a credit card balance is usually just a snowball of stress.

FAQ Section

1. Is it really possible to get a loan for expats with low interest in the first month? It’s difficult but possible if you use an international bank where you already have a relationship back home. For most people, a loan for expats with low interest requires at least 90 days of local residency and salary history.

2. Does my home country’s credit score matter? Usually, local banks can’t see it. However, specialized expat lenders and some global banks (like HSBC or Citi) may use your home score to grant you a loan for expats with low interest through cross-border data sharing.

3. What is a “Salary Transfer” loan? It is a loan where the interest rate is lower because you agree to have your salary deposited directly into the lending bank. This is often the most effective way to secure a loan for expats with low interest.

4. Are there “Early Settlement” fees? Many loan for expats with low interest offers in 2026 do not have early repayment penalties, but you must check the fine print. Being able to pay the loan off early without a fee is a huge win for your financial flexibility.

5. How much can I borrow as an expat? Typically, you can borrow between 10 to 20 times your monthly salary, provided your DTI is low. However, the largest loan for expats with low interest offers are usually reserved for those with at least one year of residency.

6. Can I get a loan for expats with low interest if I’m self-employed? This is much harder. Most lenders want to see at least two years of audited local accounts for self-employed individuals before they will consider a loan for expats with low interest.

Conclusion

At the end of the day, moving abroad is about growth—personal, professional, and financial. You shouldn’t have to sacrifice your financial health just because you changed time zones. Finding a loan for expats with low interest is about being an active participant in your own relocation strategy. It requires a bit of patience, a lot of documentation, and the willingness to shop around.