Stop paying just to use your own money! Discover the best no annual fee credit cards in 2026, maximize your cash back, and build credit without the extra costs.

Table of Contents

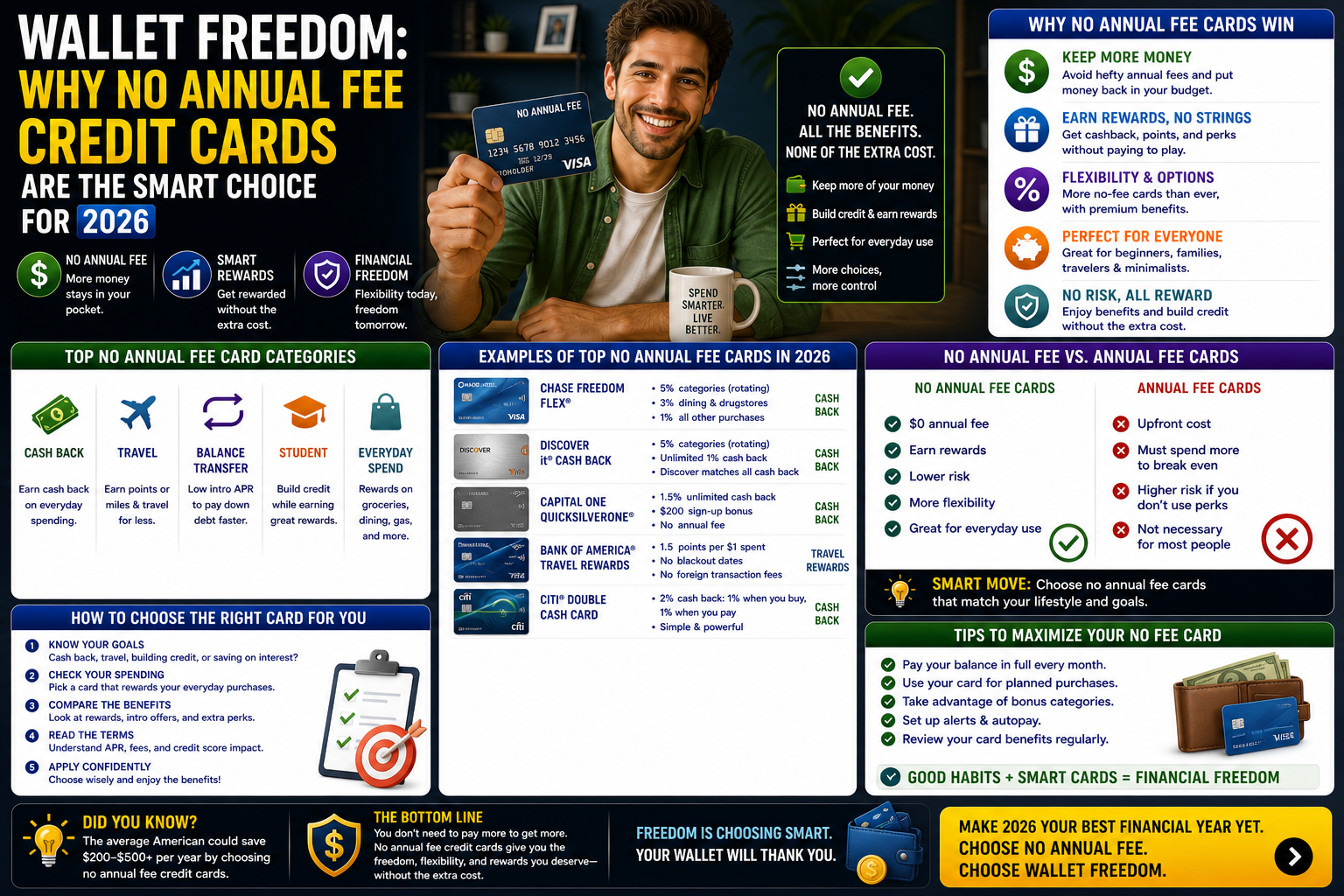

We’ve all had that moment of “billing shock.” You’re scrolling through your banking app, minding your own business, when you see a random $95 or $550 charge labeled as an “Annual Membership Fee.” It feels a bit like being charged a subscription fee just to have the privilege of spending your own hard-earned cash. For the high-flying jet-setters who live in airport lounges, those fees might make sense. But for the rest of us—people who want rewards without the overhead—the move toward no annual fee credit cards is less of a trend and more of a financial necessity.

In 2026, the credit market has shifted. Banks are hungrier than ever for loyal customers, and they are packing their entry-level products with perks that used to be reserved for the “Gold” and “Platinum” tiers. Choosing no annual fee credit cards doesn’t mean you’re settling for a “basic” experience anymore. It means you’re making a strategic decision to keep your fixed costs at zero while still reaping the benefits of cash back, purchase protection, and travel rewards. It’s about building a wallet that works for you, rather than you working to justify the cost of your wallet.

The Psychological Win of Zero-Cost Credit

There is a certain peace of mind that comes with knowing your credit line doesn’t have an expiration date on its value. When you carry no annual fee credit cards, you don’t have to do “mental math” every December to see if you earned enough points to cover the fee. If you don’t use the card for a month, it costs you nothing. If you use it every day, you’re in the black from the very first transaction.

This is particularly important for people who are just starting to build their credit history or those who want a “keeper” card they can hold onto for decades. Because the age of your accounts is a major factor in your credit score, no annual fee credit cards are the perfect anchors for a long-term financial plan. You never have to worry about closing the account just to avoid a fee, which keeps your average account age high and your score healthy.

Maximizing Cash Back Without the Overhead

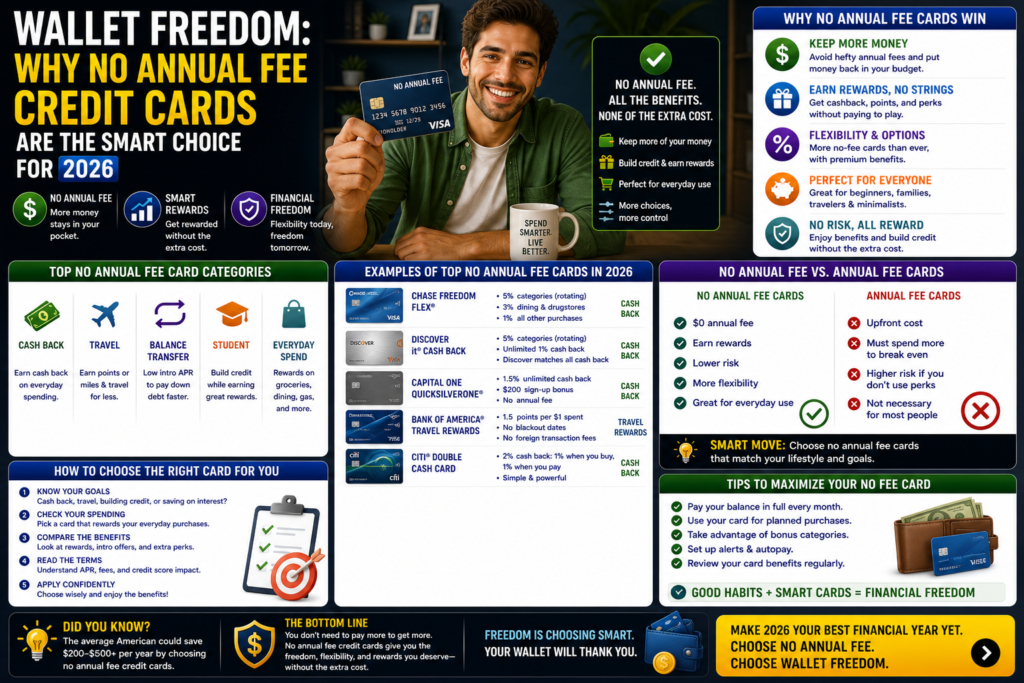

The competitive landscape in 2026 has pushed rewards rates to impressive levels. Many no annual fee credit cards now offer flat-rate cash back of 2% on every single purchase. Think about that for a second: you’re essentially getting a 2% discount on life. Whether it’s a pack of gum or a new laptop, you’re winning.

- Flat-Rate Cards: Best for people who want simplicity. No categories to track.

- Tiered Category Cards: Great for those who spend heavily on groceries, gas, or dining. Some of these no annual fee credit cards offer up to 3% or 5% in specific areas.

- Rotating Categories: For the “optimization nerds” who don’t mind activated new categories every quarter to hit that 5% ceiling.

If you’re strategic, you can pair two different no annual fee credit cards—one for your main expenses like groceries and another for everything else—to ensure you’re never earning less than 2% back. It’s a low-effort, high-reward system that doesn’t require a spreadsheets-and-calculators lifestyle.

The Secret Perks You Didn’t Know You Had

It’s a common misconception that no annual fee credit cards come stripped of all protections. In reality, many of these cards are backed by Mastercard or Visa networks that include some pretty robust “invisible” benefits. I’m talking about things like extended warranties, which can double a manufacturer’s warranty on a new appliance, or “Rental Car Collision Damage Waivers.”

When you use no annual fee credit cards to book a rental car or buy a new smartphone, you’re often getting a layer of insurance for free. I once had a friend who dropped their new phone a week after buying it; because they used a specific no-fee card that included “Cell Phone Protection,” the bank paid for the repair. Always read the “Guide to Benefits” that comes in the mail—or the PDF version in your app—because these no annual fee credit cards often have hidden features that save you hundreds of dollars in “what if” scenarios.

Travel Rewards for the Occasional Explorer

You don’t need a $695 annual fee to earn travel points. While you might not get the fancy airport lounge access, there are several no annual fee credit cards designed specifically for people who travel once or twice a year. These cards often allow you to “erase” travel purchases from your statement using points, or they offer 2x points on flights and hotels.

Another massive benefit of certain no annual fee credit cards is the absence of “Foreign Transaction Fees.” If you’re traveling to Europe or Asia, using a standard card can hit you with a 3% surcharge on every meal and souvenir. By picking the right no annual fee credit cards with 0% foreign fees, you’re essentially saving $30 for every $1,000 you spend abroad. It’s a small detail that makes a big difference in your vacation budget. To learn more about how these currency exchanges work, Wikipedia’s entry on Foreign Exchange Markets is a great place to start.

Protecting Your Credit Score for the Long Haul

As I mentioned earlier, account longevity is the secret sauce of a high credit score. When you apply for no annual fee credit cards, you are creating a permanent foundation for your credit profile. Lenders like the Consumer Financial Protection Bureau emphasize that a stable, long-term relationship with credit is a sign of a low-risk borrower.

Because there is no cost to keep the account open, you can simply tuck the card away in a drawer if your spending habits change. This keeps your “Total Credit Limit” high, which in turn keeps your “Credit Utilization” low—two of the biggest levers you can pull to hit that 800+ score. For most of us, no annual fee credit cards are the smartest way to play the credit game without being “taxed” for participating.

Navigating the “Introductory APR” Trap

One of the most powerful features of new no annual fee credit cards in 2026 is the 0% Introductory APR period. Many cards offer 12 to 18 months of zero interest on new purchases or balance transfers. This can be a godsend if you have a big expense coming up, like a wedding or a home repair.

However, you have to be disciplined. The goal is to use these no annual fee credit cards as a tool, not a crutch. If you haven’t paid off the balance by the time the intro period ends, the interest rates can jump significantly. My advice? Set up an automatic payment to clear the balance two months before the deadline. That way, you get the benefit of a “free loan” from your no annual fee credit cards without the risk of falling into a debt trap.

The Competitive Edge: Neobanks vs. Traditional Giants

The year 2026 has seen a massive influx of “Neobanks” and fintech startups offering no annual fee credit cards with incredible digital interfaces. These cards often come with real-time spending alerts, advanced budgeting tools, and the ability to “freeze” your card instantly from your phone if you misplace it.

Traditional banks have had to step up their game to compete. This “arms race” for your wallet is why we’re seeing no annual fee credit cards with perks like $5 monthly streaming credits or Uber discounts. When you’re shopping around, don’t just look at the big names like Chase or Amex. Some of the smaller players are offering the most innovative no annual fee credit cards on the market today. It’s a great time to be a consumer.

Identifying the Best Fit for Your Spending

How do you choose from the dozens of no annual fee credit cards out there? It comes down to an honest look at your monthly bank statement.

- The Foodie: Look for cards that prioritize 3% back on dining and takeout.

- The Commuter: Find a card that gives high rewards for gas or EV charging.

- The Minimalist: Go for a flat 2% cash back card and never think about categories again.

I personally believe that the “best” of the no annual fee credit cards is the one you actually use. If a card has amazing rewards but you constantly forget to activate the categories, it’s not doing you any favors. Efficiency beats optimization almost every time.

Security Features in the Modern Era

Security is a major concern for everyone in 2026. The latest no annual fee credit cards come equipped with “Tokenization” and virtual card numbers. This allows you to generate a unique card number for online shopping, so your “real” number is never exposed to potentially sketchy websites.

Even though these are no annual fee credit cards, you still get the “Zero Liability” protection. If someone steals your number and goes on a shopping spree, you aren’t on the hook for a single cent. It’s a level of security that you just don’t get with a debit card, where the money is pulled directly from your checking account. This safety alone makes carrying no annual fee credit cards worth it, even if you never use the rewards.

FAQ Section

1. Can I really get rewards with no annual fee credit cards? Absolutely. Many of the top no annual fee credit cards in 2026 offer 2% cash back or 3% on specific categories like groceries and gas. You don’t have to pay a fee to earn significant rewards anymore.

2. Is there a catch with no annual fee credit cards? The main “catch” is that these cards usually have higher interest rates than cards with fees. As long as you pay your balance in full every month, the interest rate doesn’t matter, and the card is truly free.

3. Does having no annual fee credit cards hurt my credit score? No, it actually helps. Because they are free to keep open, they help increase the “average age of accounts,” which is a major positive factor for your credit score.

4. What is a “Foreign Transaction Fee”? Some no annual fee credit cards charge a 3% fee when you buy things in a different currency. However, many modern no-fee cards have eliminated this, making them great for international travel.

5. Can I upgrade my no-fee card later? Yes. Most banks will allow you to “product change” from one of their no annual fee credit cards to a premium card with a fee if your travel needs increase later on. This usually doesn’t require a new credit check.

6. Are there welcome bonuses for no annual fee credit cards? Yes! While they aren’t as large as the $695 cards, many no annual fee credit cards offer a $200 sign-up bonus if you spend a certain amount (usually $500 to $1,000) in the first three months.

Conclusion

At the end of the day, financial health is about simplicity and efficiency. Why pay a bank for the privilege of giving them your business? By focusing your wallet on no annual fee credit cards, you’re taking a stand for your own bottom line. You’re choosing a path where every point earned is pure profit, and every perk is a genuine “thank you” from the issuer.